Review of Week 26/2023

“Try Again. Fail again. Fail better.” – Samuel Beckett

Due to other commitments, this is a short version of the newsletter that only contains a review of this week's relevant events and data. I’ll probably be sending a short version of the newsletter next weekend too (that week will be short anyway due to the July 4th holiday).

Welcome to issue #62 of fx:macro!

If you're using Gmail, you will need to click “View entire message” at the bottom since it can't display the whole thing.

The cover image is AI-generated via Midjourney. If you want to guess the prompt, I put it at the end of the newsletter.

If you like this newsletter, please consider subscribing and sharing it or forwarding it to others who might be interested. I'm also on Twitter @fxmacroguy if you want to reach out.

Table of Contents

Summary (

Playbook, Calendar, Levels,FX Drivers, Downloads)Week in Review: a) Central Banks, b) Economic Data

Market Analysis: a) Growth and Inflation, b) Yields, c) Central Banks and the US Dollar, d) Sectors and Flows, e) Sentiment and Positioning, f) Market Risks, g) VariousTop 3 Macro Charts of the Week

Summary

Currency Drivers

For an explanation check out this link.

Downloads and Links

Central bank overview with each central bank's last rate statement, press conference and minutes:

Central bank speaker recap for the week:

Week in Review

A bit of housekeeping

I will probably make a transition to a mostly PDF-based newsletter in the next couple of months. Several parts of fx:macro are already PDF-based, e.g. the central bank speaker summaries or the crib sheets before events. (The CB speakers are also included in the newsletter as text, so it's twice the work and a bit redundant.) In the future, I plan to put the Week in Review part into one PDF, and the Market Outlook into another one. There are several reasons for this:

1) A PDF is navigable and the newsletter is not, so with a PDF, I can include a proper Table of Contents with internal links and it's easy to get to a specific part, e.g. a central bank statement or a PMI.

2) Right now, I put all the images and commentary into fx:macro but I also put them into a note-taking app to have them available with the rest of my notes for the week. Again, twice the work.

3) As a reader, you can just dump every PDF into a folder on your hard drive and use full-text search (e.g. Spotlight on Mac) to search within the files, so the information is more readily available than it is right now.

4) If you're not reading the entire newsletter but only the Market Analysis, for example, it's way easier to find what you're looking for without having to go through all of the information that's not useful to you.

You can find a first version of what the weekly review could look like in PDF format below (CB speakers are not included because they already have their own PDF), and below that is the same content in the usual newsletter format. Please let me know what you think, every feedback is valuable to me!

Central Banks

BOJ Summary of Opinions (26.06.23)

There were two key paragraphs in the SOP: one that says core CPI probably won't fall below 2% and one that says a revision to YCC should be discussed “at an early stage”:

Here are a few more bullet points:

Factors behind significant improvement since April in households' sentiment indicators include the achievement of wage increases at high levels.

It is necessary to assess whether there is a higher possibility of achieving wage increases that can keep up with inflation.

The y/y increase in CPI is likely to decelerate toward the middle of fiscal 2023. Meanwhile, there are still high uncertainties over whether it will accelerate again thereafter.

While price rises in Japan are still largely attributable to overseas factors, the contribution of domestic factors has increased.

Inflationary pressure is likely to remain strong for the time being.

The y/y increase in CPI is expected to fall below 2% in the second half of fiscal 2023.

Corporate behavior has seen clear changes, and price and wage hikes have been incorporated into corporate strategy. In addition, various measures of underlying inflation have mostly shown a rate exceeding 2%. It is highly likely that the y/y increase in the CPI (all items less fresh food) will decelerate toward the middle of fiscal 2023 but will not fall below 2 percent.

Given the outlook for prices and other factors, it is appropriate that the Bank continue with the current monetary easing.

The wage growth rate agreed in this year's annual spring labor-management wage negotiations thus far has been the highest in around 30 years. It would be premature to revise monetary policy if it would hinder such developments.

There is no need to revise the conduct of yield curve control.

The functioning of the bond market has improved compared with a while ago, but its level has remained low.

A revision to the treatment of yield curve control should be discussed at an early stage.

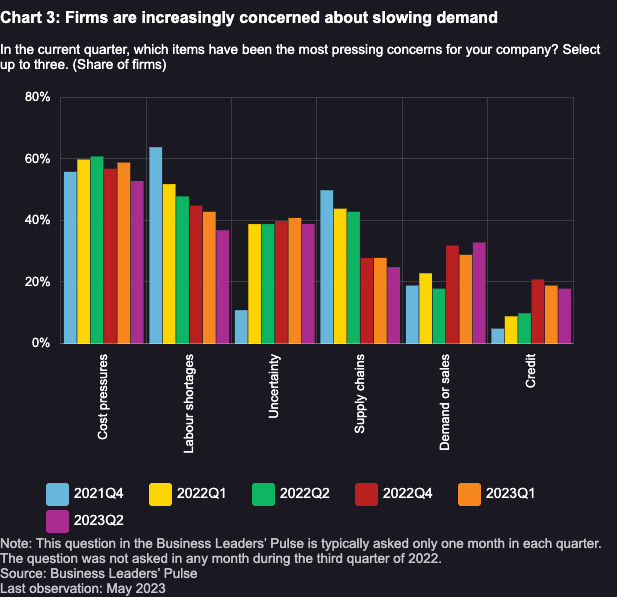

BOC Business Outlook Survey (30.06.23)

The decrease in the BOS indicator mainly reflects:

more businesses expecting slower price growth

weaker hiring and investment intentions

broader tightening in credit conditions

eased capacity pressures, particularly related to supply chain bottlenecks

The continued fall in the BOS indicator signals less inflationary pressure than in recent quarters.

Slowing demand has become a more important and widespread concern in recent quarters. Despite this, fewer firms expect an outright recession: one-third of firms participating in this quarter’s BOS are planning for a recession, compared with one-half in the first quarter.

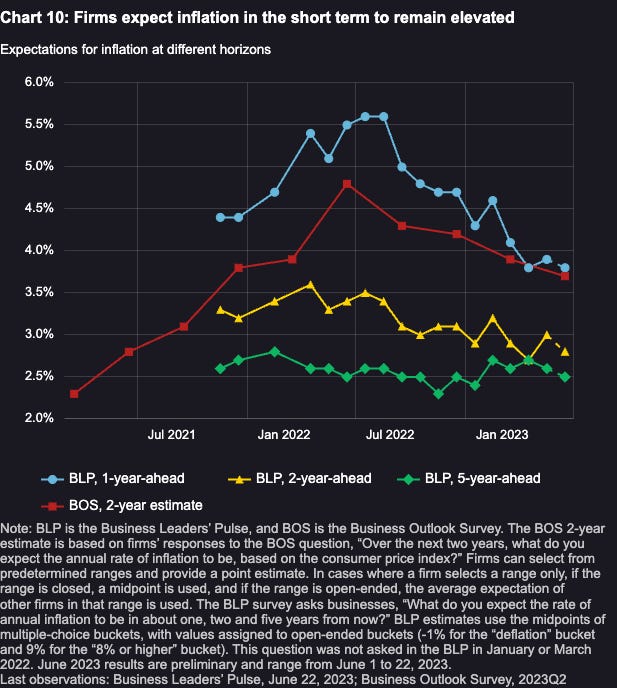

Firms’ expectations for inflation in the short term have edged down again but continue to be elevated. Businesses most commonly attribute short-term inflationary pressures to high labour costs, robust government spending and a strong domestic economy. In contrast, 3 in 10 firms anticipate that inflation will soften to between 2% and 3% on average over the next two years. These businesses attributed their expectations of weaker inflation to monetary policy actions that the Bank has taken throughout the past 15 months.

Overall, firms still expect inflation in the long term to be within the Bank’s inflation-control target range. However, several businesses—more than in recent surveys—think it will take five years or longer for inflation to return to the Bank’s 2% target.

Confab, Speakers, News

Federal Reserve

Williams (Neutral). Mon: Restoring price stability is of "paramount importance".

Powell (Neutral). Wed: We believe there is more restrictive policy coming, policy hasn't been restrictive for very long, have not made a decision to hike at every other meeting, would not take moving at consecutive meetings off the table, data over the last quarter has been strong, as we get closer and close to the goal the risks become more balanced, haven't seen much progress in non-housing services, high labour costs in non-housing services are causing inflationary pressures, need to see more softening in the labour market. Thu: The process of getting to 2% inflation target has a long way to go, expects moderate pace of interest rate decisions to continue, a strong majority of the FOMC expects it to be appropriate to hike rates two or more times by the end of the year, inflation is well above the goal, the xtent of effects from tighter credit conditions remains uncertain, will take time for the rest of the economy to feel the full impact of rate hikes so far, the labour market is very tight.

Bostic (Neutral). Thu: I don't see as much urgency to move as stated by others, nobody should take a signal from my view that we should pause, we're not seeing inflation moving away from target, comfortable waiting, there are undoubtedly scenarios where we could move at two meetings in a row but not expecting that will happen, will do more if needed, less concerned about high inflation. Thu (again): Not ready to rule out further rate hikes if required but does not see need, does not see Fed rate cuts in 2023 or 2024, monetary policy has only recently moved into restrictive territory, effects of monetary policy tightening are starting to show up in the real economy, policy in place to bring inflation back to 2% target, it's unambiguous that inflation has fallen considerably, inflation is in a gradual cooling trend that should continue, inflation should cool even if Fed leaves current policy in place, expects to reach inflation goal without causing severe downturn.

Goolsbee (Neutral). Fri: There is nothing in the Fed's mandate about stock prices, I hope the market remains sober, have to see through the market's ups and downs, have not made up my mind on rates, there is a number of data releases before the next Fed meeting, there is a lag in the impact of interest rates on the economy, hopeful we can get inflation down to target without a recession, the strongest part of the economic data is the labour market.

European Central Bank

De Guindos (Dove). Weekend: Monetary policy measures are starting to have an impact on financing conditions, a contraction in credit will pass through to the real economy with dampening demand to lower inflation, the finishing line is in sight in response to a question if the target is a long way off, if an end to rate hikes can be expected before the summer holidays will depend on the incoming data. Wed: There is more ground to cover on rates, July rate hike is set.

Makhlouf. Weekend: Undecided regarding a rate increase beyond July, prepared to look at the evidence.

Simkus (Hawk). Mon: At least one more rate hike is required. Tue: We are not done with hiking rates, should not rule out the option of a hike in September but too early to say, must keep rates restrictive to reach 2% inflation target.

Kazaks (Hawk). Tue: Market pricing of rate cuts in early 2024 is wrong, sees rate hikes past July but when and by how much will be data dependent, doesn't think that in July we'll be comfortable enough to say we're done, there are still strong risks of persistence in inflation.

Lagarde (Dove). Tue: We need to bring rates to "sufficiently restrictive" territory, need to communicate clearly that we'll stay at those levels for as long as necessary, we have not yet seen the full impact of the cumulative rate hikes since last July, not likely to say with full confidence that rates have peaked, we are committed to reaching inflation target come what may, we cannot waver and declare victory yet. Wed: We will very likely hike again in July, for September we are data dependent, we still have ground to cover, not seeing enough tangible evidence of stabilizing domestic inflation, the European economy is stagnant at best, manufacturing does not give great hope for a strong recovery, our baseline does not include a recession, transmission of monetary policy will be slower because there are more fixed-rate mortgages.

Wunsch (Neutral). Tue: A rate pause would need a clear signal of slowing core inflation, staflation is the base case, more action is needed if core does not moderate, we must accept that our ability to fix inflation at exactly 2% is limited, wouldn't tighten monetary policy if inflation was at 2.3% and the economy was weak.

Vasle. Wed: We need to keep tightening policy at our next meeting, beyond that we will remain data dependent, the burden of proof will be on invalidating a rate hike rather than validating one, inflation remains persistent.

Vujcic. Wed: There is a good chance of a September rate hike, we can engineer a soft landing.

Müller. Wed: Too early to say where rates will end up, we need to look at the data for a rate hike beyond July, rate hikes are gradually having an impact, risks to inflation are still on the upside.

Centeno. Wed: Inflation is easing as quickly as it went up, over-tightening is not an acceptable position, the economy is already taking a hit and inflation will react, we are definitely getting to the terminal rate. Thu: We are reaching the time when monetary policy can pause, we are very close, not overreacting is a huge concern for every central bank.

Villeroy. Wed: We need to be sufficiently patient on the duration rates are kept high, we are closer to terminal levels of rates, need to be more cautious about forward guidance but would not throw it away completely, inflation expectations remain well anchored, more confident on a soft landing but not without pain, expects a catch up in real wages and not a price spiral.

De Cos (Dove). Thu: September meeting decision is absolutely open.

Makhlouf. Fri: We've seen a greater persistence in inflation, inflation is stickier, the decision when to stop raising rates is not straightforward, we're near the top of the ladder.

Sources. Mon: Econostream: there is a decent chance of another rate hike at the September meeting, even greater agreement that market pricing for when a rate cut will occur is unreasonably optimistic. Tue: A rate pause would need a clear signal of slowing core inflation, staflation is the base case, more action is needed if core does not moderate, we must accept that our ability to fix inflation at exactly 2% is limited, wouldn't tighten monetary policy if inflation was at 2.3% and the economy was weak. Wed: Bloomberg: Officials are considering a faster reduction of the ECB bond portfolio. Econostream: ECB insiders are "reasonably relaxed" about the current pace of QT, passive runoff is sufficient "for now".

Bank of England

Dhingra (Dove). Tue: UK wages are responding to inflation with a lag, sharp drop in PPI is promising, there is a lag between fall in PPI and CPI of around one or two quarters.

Bailey (Neutral). Wed: Data showed a clear persistence of inflation, will be "evidence driven", will do what is necessary, expects inflation to come down, not getting inflation back to target is a worse outcome, labour market in the UK is very very robust, the labour force is smaller than at the outbreak of Covid, the economy has turned out to be much more resilient so far.

Tenreyro (Dove). Thu: My vote to leave bank rate unchanged at my final policy meeting rested on what the latest data implied about the medium term, forward-looking indicators had pointed towards falls in both pay growth and core-goods inflation, tightening already in the pipeline would be sufficient to bring inflation below the target.

Swiss National Bank

Jordan. Weekend: The recent interest rate hike was "very likely not quite" enough to come fully to grips with the high rate of Swiss inflation.

Maechler. Wed: Inflation is more persistent than we anticipated, inflation is becoming more broad-based in Switzerland, over 65% of all goods and services are seeing price increases, long-term inflation expectations have remained anchored below 2%.

Bank of Japan

Kanda. Mon: Will respond to FX moves if they become excessive, FX should move stably reflecting fundamentals, will not rule out any options on intervention, we are focusing on moves rather than levels. Wed: Closely monitoring FX market moves with a high sense of urgency, will take appropriate action in excessive moves.

Suzuki. Mon: Will respond appropriately if there are excessive FX moves, will continue to watch the FX market with a sense of urgency. Wed: Will respond appropriately to excessive FX moves if necessary, one-sided movement seen in the current market, no comment on FX levels. Thu: Closely watching FX moves, one-sided moves are undesirable, won't rule out any options if FX moves are excessive, no comment on FX levels. Fri: Sharp and one-sided moves seen in FX market, the exchange rate should move stably reflecting fundamentals, closely watching with a great sense of urgency, will respond appropriately if moves become excessive.

Matsuno. Mon: Closely watching FX moves with a high sense of urgency, important for the exchange rate to move stably reflecting economic fundamentals, seeing sudden and one-sided moves in the FX market. Fri: Closely watching FX moves with a high sense of urgency, sharp and one-sided moves seen recently, will take appropriate steps on excessive FX moves, important for the exchange rate to move stably reflecting economic fundamentals.

Ueda. Wed: Underlying inflation is still below 2%, wage inflation is now running at around 2% so there's some ground to cover, if we become reasonably sure about the second part of inflation forecasts that would be a good reason for reconsidering a policy change, if we do get to normalize our monetary policy then rates may go up by a large margin and we will have to be careful and carry out all kinds of stress tests, we think the economy is going to expand at slightly-above potential for some time, demographics are working to tighten the labour market for quite a long while, we haven't had any serious policy tightening in decades.

Himino. Thu: BOJ must scrutinize newly emerging factors that are pushing up prices, recent rises in Japan's CPI are more modest than in the US and Europe but stronger than previously expected, not seeing signs of risk Japan would experience too-high inflation.

People's Bank of China

Unknown. Fri: To implement prudent monetary policy accurately and forcefully, to effectively support domestic demand expansion and improve private consumption environment, to ensure delivery of housing and promote healthy development of the real estate market, to keep liquidity reasonably ample and also maintain reasonable credit growth.

Economic Data

Monday, 26.06.23

Tuesday, 27.06.23

Wednesday, 28.06.23

Thursday, 29.06.23

Friday, 30.06.23

Links to relevant central bank releases in previous editions of this newsletter:

Fed

FOMC Statements: 25/2023 | 19/2023 | 13/2023 | 06/2023 | 50/2022 | 45/2022 | 39/2022 | 31/2022 FOMC Meeting Minutes: 22/2023 | 15/2023 | 09/2023 | 02/2023 | 47/2022 | 42/2022 | 34/2022 | 28/2022 | 25/2022 Crib Sheets: 05/2023 | 50/2022 | 37/2022

ECB

Rate Statements: 25/2023 | 19/2023 | 12/2023 | 06/2023 | 50/2022 | 44/2022 | 37/2022 | 30/2022 Meeting Minutes: 22/2023 | 17/2023 | 10/2023 | 04/2023 | 47/2022 | 35/2022 | 28/2022 | 21/2022 Economic Forecasts: 21/2022 Crib Sheets: 11/2023 | 05/2023 | 50/2022 | 43/2022 | 36/2022

BOE

Rate Statements: 25/2023 | 20/2023 | 13/2023 | 06/2023 | 50/2022 | 45/2022 | 39/2022 | 32/2022 | 25/2022 Financial Stability Reports: 28/2022 Crib Sheets: 05/2023 | 50/2022 | 37/2022

RBA

Rate Statements: 24/2023 | 19/2023 | 15/2023 | 11/2023 | 07/2023 | 50/2022 | 45/2022 | 41/2022 |37/2022 | 32/2022 | 28/2022 Meeting Minutes: 25/2023 | 21/2023 | 17/2023 | 09/2023 | 51/2022 | 47/2022 | 43/2022 | 39/2022 | 34/2022 | 30/2022 | 26/2022 | 21/2022 Statements on Monetary Policy: 19/2023 | 07/2023 | 45/2022 | 32/2022 Crib Sheets: 40/2022 Financial Stability Reports: 41/2022

RBNZ

Rate Statements: 22/2023 | 15/2023 | 09/2023 | 47/2022 | 41/2022 | 34/2022 Meeting Minutes: 07/2023 Crib Sheets: 40/2022

BOC

Rate Statements: 24/2023| 15/2023 | 11/2023 | 05/2023 | 50/2022 | 44/2022 | 37/2022 Crib Sheets: 43/2022 | 36/2022 Summary of Deliberations: 25/2023 | 18/2023

SNB

Rate Statements: 25/2023 | 13/2023 | 50/2022 | 44/2022 | 39/2022 | 25/2022 Crib Sheets: 50/2022 | 37/2022

BOJ

Rate Statements: 25/2023 | 18/2023 | 11/2023 | 04/2023 | 51/2022 | 39/2022 | 30/2022 | 25/2022 Summary of Opinions: 20/2023 | 13/2023 | 05/2023 | 52/2022 | 46/2022 | 41/2022 | 31/2022 Crib Sheets: 43/2022

Photo Credit: 4th of july fireworks, clip art, white background

thank you, great take!

Great stuff as always, I’m interested to watch when the BoJ intervenes in the FX markets. The PDF transition is something i’m a fan of!