Correlation Heatmap

Please note that this should still be considered a work in progress or a beta version. If you find any bugs or have any suggestions, please don't hesitate to contact me.

If you want to learn how to build this yourself, check out my free guide:

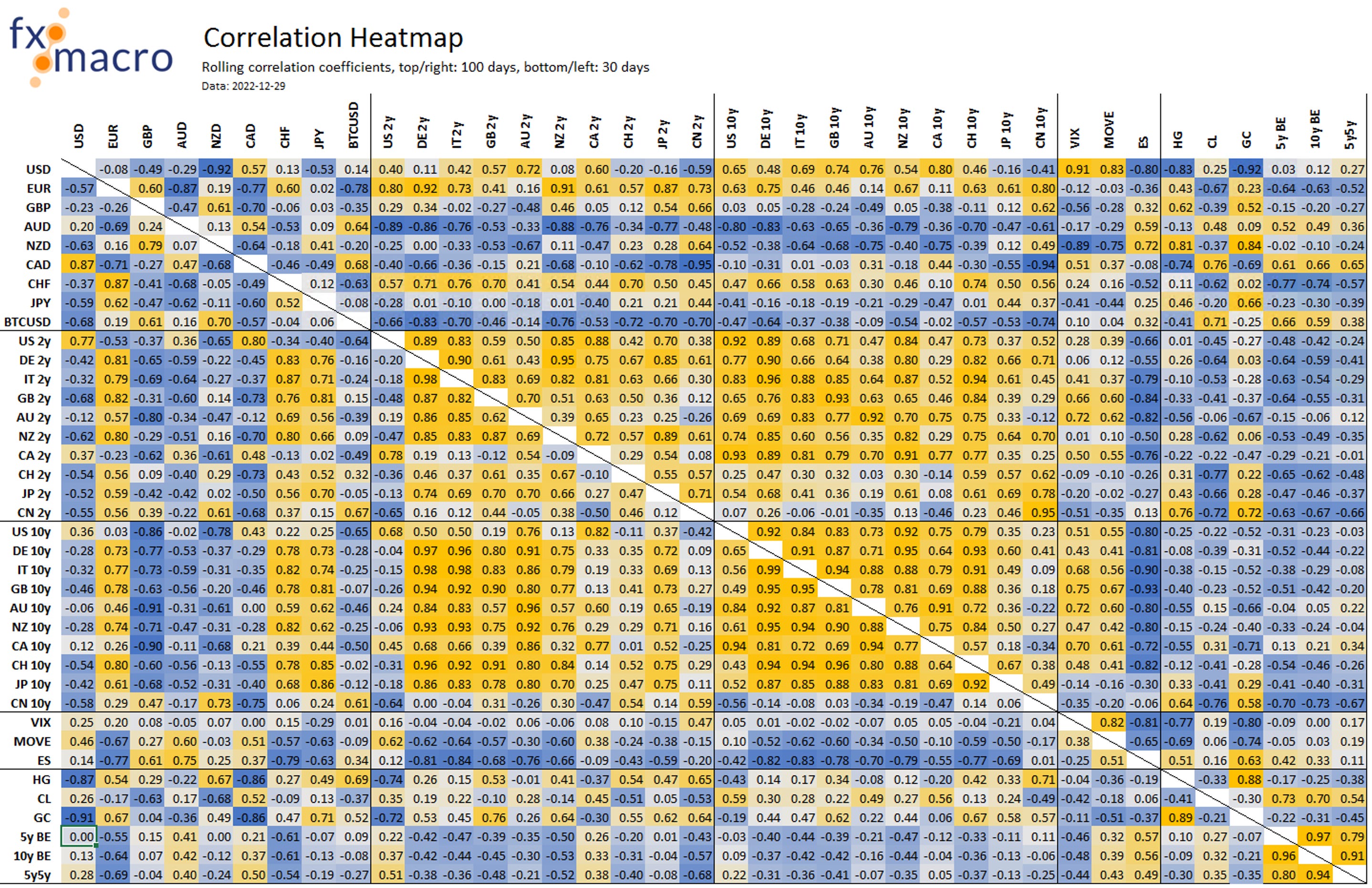

The Correlation Heatmap is one of the tools I use to find out what drives what (and what doesn't) at the moment. Here's what it looks like:

Note the diagonal line going from the top left to the bottom right. It's dividing the map into two sections that show different data: the top/right shows a rolling 100-day correlation, and the bottom/left shows a rolling 30-day correlation.

Since this is a pretty exhaustive thing to go through and there are a few different correlations I'm always interested in, I put that together in a handy little cheat sheet:

Each currency vs. its own 2y and 10y yields as well as its 2s10s,

each currency vs. the ES and the VIX,

each currency vs. their own domestic stock market, and

some special correlations for several currencies.

The top row shows the 30-day correlation, and the row below shows the 100-day correlation.

Here are some examples of what I can learn from this and why it's valuable to me: right now…

EUR and JPY both show very high short-term correlation with their 2s (not surprising given the recent actions of the ECB and the BOJ),

The correlation between JPY and its 10s has gone up from 0.44 at 100 days to 0.86 over 30 days (which is also what I would have expected given the BOJs latest decision),

The USD has a very high negative 100-day correlation of -0.80 to the ES but it's uncorrelated to EUR (-0.08),

JPY strength is (as expected) negative for the Nikkei (30-day correlation at -0.89),

EUR and BTPBUND have been negatively correlated over the last 100 days but that has switched to +0.78 over the last 30 days,

AUD and Iron Ore have fallen out of love, AUD and GC are uncorrelated at the moment,

AUD and NZD are completely uncorrelated,

CAD goes where USD goes (+0.87 and +0.57 over 30 and 100 days, respectively).