Review of Week 43/2022

Just the review part this week... watch out for a Twitter thread.

⚠️⚠️⚠️

Due to unforeseen circumstances that came up on very short notice (i.e. this morning), I will not be able to publish the full newsletter this weekend. Below you’ll find the weekly recap. I will put together a Twitter thread today or tomorrow with a short market outlook and should be back with a regular issue of fx:macro next weekend.

⚠️⚠️⚠️

Welcome to issue #28 of fx:macro!

If you like this newsletter, please consider subscribing and sharing it or forwarding it to others who might be interested. I'm also on Twitter @fxmacroguy if you want to reach out.

One more thing. You seem to like newsletters, so here's a great way to discover new stuff to read for free: The Sample. They will regularly send you an issue of a different semi-random newsletter you might be interested in. If you sign up using my referral link, I get bonus points and my newsletter will be forwarded to others to check out.

Before diving in, I’d like to shout out to The Morning Hark!

For me, it’s a must-read every day. Here’s what’s in it:

Overnight action in key asset classes including commodities, fixed income and crypto,

Current macro themes with a review of the previous day’s economic data releases, central bank speakers and more,

Main highlights ahead with a comprehensive list of upcoming data and events,

The top 5 trending posts on app.harkster.com, and

A section with links to more in-depth pieces or useful information on current macro themes.

The Morning Hark is a great way to stay on top of what’s going on in markets. If you like fx:macro, you will love The Morning Hark, so check it out!

Table of Contents

Summary (

Playbook, Calendar, Levels,Downloads)Week in Review

Central Banks

Economic Data

Market AnalysisGrowth and InflationYieldsCentral BanksSectors and FlowsSentiment and PositioningMarket RisksVarious

Other Stuff I've been looking at

Summary

Downloads and Links

Central bank speaker recap for the week:

Central bank speaker recap for next week’s CB events:

Week in Review

Central Banks

RBA Meeting Minutes (18.10.)

The RBA explained their recent dovish 25 bps hike in a bit more detail:

The decision between 25 and 50 bps was “considered carefully” and was a “finely balanced” one

25 bps won out because:

Monetary policy operates with a lag

Risk of household spending adjusting more than expected

Increases in the cash rate are close to the interest rate buffer applied when many borrowers took out their loans (i.e. mortgages)

Wage growth has not yet reached a level consistent with the inflation target, some further rises in wage growth would not be a concern

Other central banks that take larger hikes meet less frequently than the RBA

Confab, Speakers, News

Federal Reserve

Bullard (Hawk). Weekend: 75 bps rate hikes have not caused market turmoil, front-loading is the correct strategy, we have a serious inflation issue. Wed: The Fed should not react to declines in the stock market, not clear equity pricing should be the main metric of financial liquidity, there does not appear to be a lot of financial stress in the economy, have to get to right level of rates and then move to data-dependency, if inflation starts to decline meaningfully in 2023 the Fed can stay at higher rate level. Fri: Job market is extremely strong and allows the Fed to fight inflation, hoping to start disinflationary process in 2023, wants rates that put significant downward pressure on inflation, minor adjustments can be made going forward, wouldn't call lower equity prices financial stress.

Bostic (Dove). Tue: Fed cannot solve all problems causing current inflation.

Kashkari (Dove). Tue: Fed needs to do much more without help from the supply side, could easily see rates getting to mid-4% next year or even higher if there's no progress on inflation, so far there's no evidence of a peak in inflation, not ready to declare pause in rate hikes until some compelling evidence core inflation has at least peaked. Wed: Risk of undershooting on rate hikes is bigger than overdoing it, best guess is the Fed can pause hikes sometime next year, little evidence of labour market softening, hard to get a firm read on the economy, possible that headline inflation has peaked but no evidence core inflation has peaked, it takes a year or two for hikes to work through the economy.

Evans (Neutral). Wed: If the Fed can keep unemployment below 5% that would be "unusual and good", FFR at 4.50-4.75 would be appropriate, mindful of Fed's impact on the economy but inflation remains the main job, Fed policy must be suitably restrictive, if the Fed pushes policy further than planned it could weigh on the economy, need to make sure inflation pressures don't broaden further. Fri: Will need to raise rates further and hold for a while, will need a period of restrictive financial conditions, sees FFR a bit above 4.5% by early 2023, labour market remains strong.

Harker (Neutral). Thu: FFR likely well above 4% by year-end, will keep raising rates "for a while", policy needs to be restrictive for a time, can stop hiking sometime next year to assess policy impact, need to see sustained drop in inflation to change policy outlook, progress on lowering inflation has been disappointing. GDP likely flat this year, 1.5% next year, inflation to fall to around 4% next year, unemployment to rise to 4.5% next year.

Cook (Neutral). Thu: Ongoing rate hikes are likely required.

Daly (Neutral). Fri: More tightening is needed, slowing hikes should be considered at this point, important to step down hikes to 50 or 25 bps hikes at some point but not a pause, might have another 75 bps hike but not going to be 75 bps forever, 4.5-5% FFR next year is reasonable, can easily find yourself overtightening, wants to avoid an "unforced downturn" by overtightening, SEP projections are a fairly good reflection of own expectations. Estimates neutral at 3-3.5%. Have to take global factors into account.

European Central Bank

Nagel (Hawk). Weekend: We need several more rate hikes and must not relent too soon, ECB should consider reducing its asset holding, Germany is facing a large and long-term decline in economic output.

Knot (Hawk). Weekend: Convinced interest rates have to rise above neutral, once rates reach neutral level it makes sense to consider running off APP stock.

Lane. Weekend: We need rate increases at the next several meetings, not trying to be overly precise on target for interest rates.

De Guindos (Dove). Mon: Expects the dollar to stabilize in the coming months.

Herodotou. Tue: ECB needs to raise rates several more times, targeting inflation over the medium term, it can take up to 18 months for policy to filter through, no signs of wage-price spirals in Europe so far.

Makhlouf. Tue: Raising interest rates is absolutely necessary, Eurozone may be facing a recession, history teaches us that situation will only be exacerbated if we delay action.

Stournas. Fri: Wage growth in the Eurozone remains relatively muted, few signs that a wage-price spiral could develop.

Bank of England

Bailey (Neutral). Weekend: Will not hesitate to raise rates in order to fulfil inflation objective, inflation should peak at roughly 11%, inflationary pressures will necessitate a bigger response than we anticipated in August. Does not normally want to comment on fiscal policy but must highlight sustainability.

Cunliffe (Dove). Wed: Will set out terms for selling bonds bought after mini-budget at the right time, monetary policy needs to do what its needs to do. LDI funds can absorb a 200 bps rise in yields, weaker areas particularly in non-bank finance and especially in emerging markets, Dutch central bank looking at what's happening in the UK on LDI. Government power to call in, rewrite, veto financial rules made by regulators would be a serious concern, would affect perception of independence of BOE's regulatory part. Did not have a full briefing on mini-budget before its announcement.

Hauser (Director of Markets). Wed: Fallout in gilt markets after mini-budget was a "full-scale liquidation event" for pension funds. Could take five to ten years to unwind QE, exit for bonds bought after mini-budget might be more straightforward than for QE stock.

Broadbent (Neutral). Thu: Justification for tighter policy is clear, market pricing of bank rate path implies pretty material hit to demand, whether rates have to rise as much as currently priced in remains to be seen.

Statement. Mon: Gilt buying operation has enabled a significant increase in resilience of the sector, TECRF (temporary expanded collateral repo facility) will remain available until November 10. The BOE will resume corporate bond sales next week. Tue: Markets may remain volatile in coming weeks, LDI funds are now better prepared for similar shocks in the future, risk of LDI funds creating a fire sale and self-reinforcing falls in gilt prices has been reduced significantly. Tue: First gilt sale re-scheduled to November 1 in light of government's fiscal announcement on October 31, expects similar size and frequency of sales as has been previously announced. Thu: The first gilt sales will start on November 1 and run until December 8, focus will be on short- and medium-dated bonds only.

Reserve Bank of Australia

Bullock. Tue: Expects further rate increases over coming months, pace and timing depend on data, determined to do what is necessary to return inflation to target, can achieve similar tightening with smaller individual rate rises because the RBA is meeting more often than its peers, size of October rate hike was actively discussed internally at the Board meeting.

Bank of Japan

Suzuki (FinMin). Weekend: We remain committed to acting decisively in the event of excessive FX volatility. Mon: Will take decisive action against FX moves that are based on speculation, constantly watching FX movements with a sense of urgency. Tue: Closely watching FX moves with a sense of urgency, cannot tolerate excessive FX moves driven by speculation, will respond appropriately, no comment on stealth intervention, won't disclose FX interventions every time. Wed: Watching exchange rate closely with a sense of urgency, cannot tolerate excess FX volatility backed by speculative moves, will take appropriate steps. Thu: Will take action against any speculative, excessive and sudden moves; no comment on FX levels. Fri: Facing speculators severely, monetary policy is up to the BOJ, public finances haven't suddenly turned for the worse to cause yen weakening, striving to achieve primary budget balancing target.

Kuroda. Weekend: Continuing with monetary easing since Japan's headline inflation is likely to decline below 2% next fiscal year. Mon: CPI to fall short of 2% in fiscal year 2023, appropriate to continue with monetary easing. Tue: Extremely important for FX to move stably, reflecting economic fundamentals, sharp and one-sided weakening not desirable for the economy. Wed: Extremely important for FX to move stably, reflecting economic fundamentals, sharp and one-sided weakening not desirable for the economy, monetary policy does not directly target exchange rate, CPI likely to fall below 2% next year. Fri: Japan's economy is looking better than during the pandemic, will continue with current monetary policy to achieve inflation target stably, must closely watch impact of FX markets on domestic economy and prices.

Wakatabe. Weekend: We haven't modified our policy stance at all, Japan's underlying inflation is too low.

Kanda (FX diplomat). Mon: Will respond firmly to excessive FX moves. Thu: Always ready to take action in FX market, will not comment on specific FX levels or whether we are intervening right now or have intervened today. Fri: Would not comment on FX intervention even if we had done it.

Kishida (PM). Mon: Specific monetary policy is up to the BOJ to decide, not commenting on FX levels. Will pick the most appropriate person to succeed Kuroda in April next year. Tue: Speculative-driven rapid FX moves are problematic, prepared to take appropriate action as needed, no comment on specific exchange rate, will work closely with the BOJ. Wed: Need to take appropriate action on excessive FX moves, excess volatility based on speculation cannot be tolerated, no comment on specific exchange rate.

Matsuno (Chief Cabinet Secretary). Tue: Closely watching FX moves with a sense of urgency, will take appropriate steps on excessive FX moves, no comment on day-to-day moves.

Adachi. Wed: Inflation starting to rise but not convinced target will be achieved in a stable and sustained manner, responding to short-term FX moves would heighten uncertainty.

Yamagiwa (EconMin). Fri: Sharp FX moves are undesirable.

Economic Data

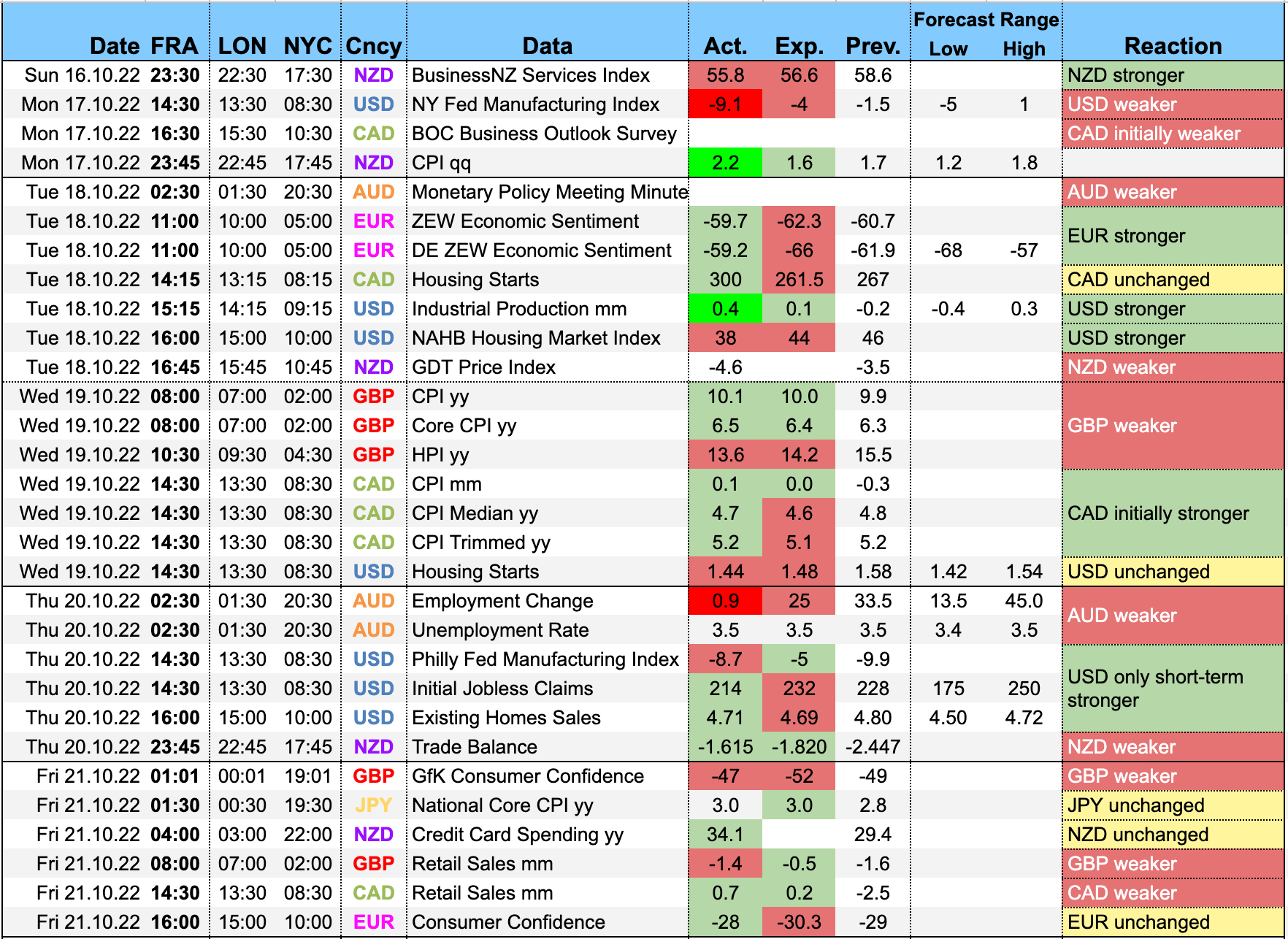

Monday, 17.10.22

Tuesday, 18.10.22

Wednesday, 19.10.22

Thursday, 20.10.22

Friday, 21.10.22

Links to relevant central bank releases in previous editions of this newsletter:

Thank you for the review, appreciate!