Review of Week 22/2023

"Beware of trading quotes" - Andreas Clenow

This week's edition will be a short one with the review part only. We'll be back with a regular issue next week.

Before we start: I'm thinking about making some changes to fx:macro in the next few months, and one of them might be a transition from ultra-long text-based emails to a more long-form friendly format. I'd be grateful if you could you'd tell me your preference:

Welcome to issue #58 of fx:macro!

If you're using Gmail, you will need to click “View entire message” at the bottom since it can't display the whole thing.

The cover image is AI-generated via Midjourney. If you want to guess the prompt, I put it at the end of the newsletter.

If you like this newsletter, please consider subscribing and sharing it or forwarding it to others who might be interested. I'm also on Twitter @fxmacroguy if you want to reach out.

Table of Contents

Summary (

Playbook,Calendar,Levels,FX Drivers, Downloads)Week in Review: a) Central Banks, b) Economic Data

Market Analysis: a) Growth and Inflation, b) Yields, c) Central Banks and the US Dollar, d) Sectors and Flows, e) Sentiment and Positioning, f) Market Risks, g) VariousTop 3 Macro Charts of the Week

Summary

Economic Calendar for next week

If you want a quick and easy way to hook a customized economic calendar into your favourite calendar app then check out this link.

Currency Drivers

For an explanation check out this link.

Downloads and Links

Central bank speaker recap for the week:

Week in Review

Central Banks

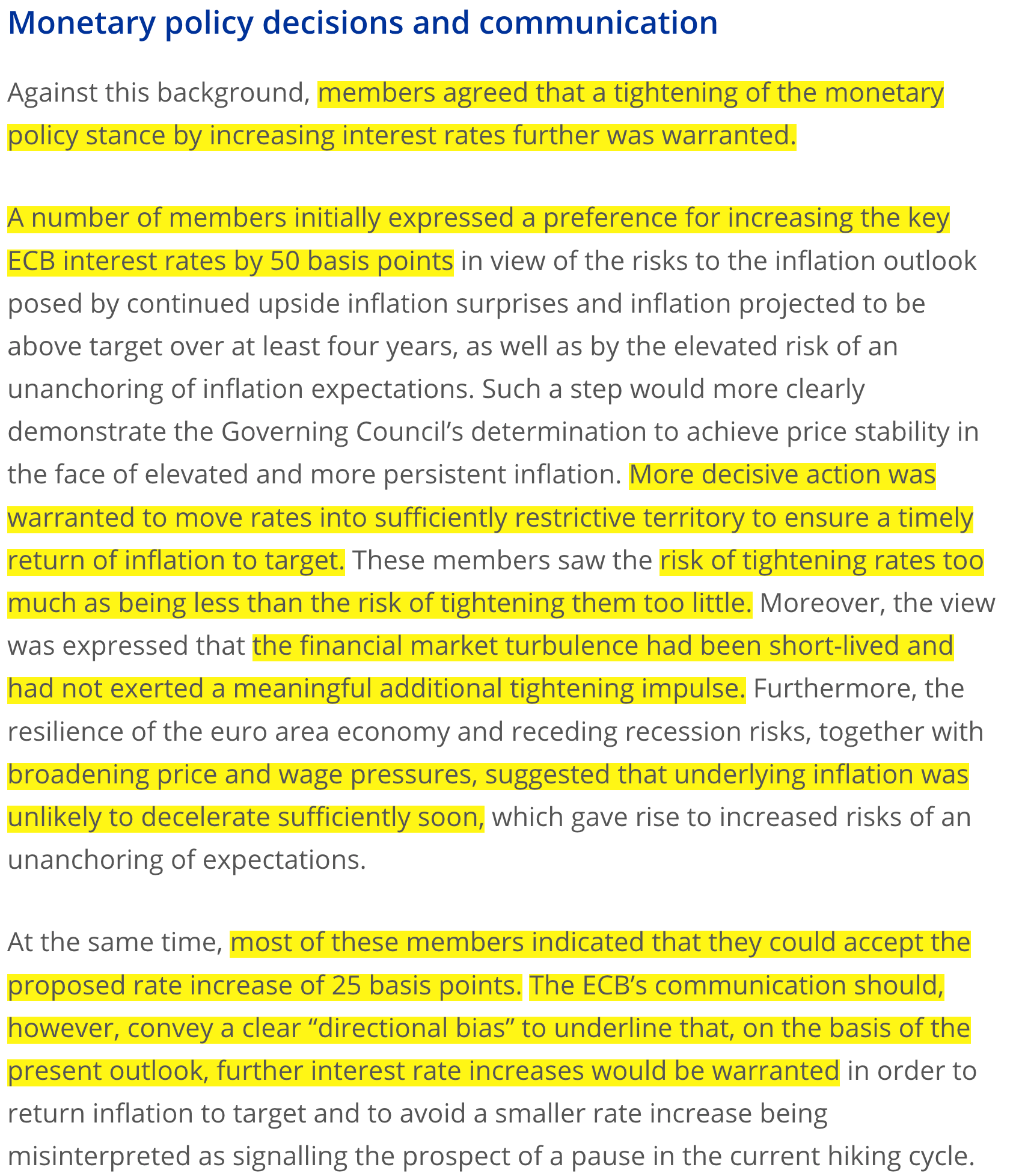

ECB Minutes (01.06.23)

The ECB Minutes were quite a hawkish read with concerns about entrenched inflation, a beginning wage-price spiral and “social conflict between workers and employers” about high inflation. Here are the highlights from the section on the policy decision:

Confab, Speakers, News

Federal Reserve

Goolsbee (Neutral). Weekend: Trying to make it a point not to prejudge and make decision when we're still weeks out from the next FOMC meeting, we are going to get a lot of important data between now and then.

Barkin (Neutral). Tue: There is uncertainty around where rates need to go, it would be shocking if rates fell again to zero in a future recession, hopes that rates can stat at a "neutral, normal" level for some time, seeing evidence that rate hikes are curbing demand, CRE strain appears focused in B and C quality office buildings in downtown areas and not the entire sector.

Mester (Hawk). Wed: No compelling reason to wait on rate hikes, more of a compelling case for bringing rates up and then holding for a while, decision could still be swayed by NFP and the next inflation report.

Bowman (Neutral). Wed: Residential real estate appears to be rebounding with implications for the Fed's inflation battle, while lower rents will eventually be reflected in inflation data home prices themselves are levelling out.

Collins (Neutral). Wed: Inflation is simply too high, the Fed is intent on reducing inflation.

Jefferson (Neutral). Wed: Skipping a rate increase at the coming meeting would allow us to see more data before deciding on the extent of additional tightening, holding rates constant should not be taken to mean rates have reached a peak for this tightening cycle, inflation remains too high but some measures have been slowing, monetary policy works with a lag and a year is not long enough to feel the full effect, base case outlook is not for a recession.

Harker (Neutral). Wed: I am in the camp that we can skip a meeting, it would be a skip and not a pause, a pause says you may hold there for a while and I don't know that we're ready for that yet, data still to come may change my mind, need some slowing in the labour market, the economy keeps chugging along, not seeing much of a credit crunch after SVB. Thu: My preference is for skipping a rate hike, it's prudent to skip a rate hike in June, let's skip and see how it goes, we are close to the place where we can hold rates in place, sees promising signs that the Fed's rate hikes are working, disinflation is disappointingly slow, if inflation started coming down unexpectedly fast then we could cut rates but that is not my forecast, sees 2023 GDP growth below 1% and unemployment at 4.4%, expects inflation to fall to around 3.5% this year and 2.5% next year with 2% in 2025.

Bullard (Hawk). Thu: Rates are at the low end of what is arguably sufficiently restrictive, monetary policy landscape in much better shape today with the FFR at a more appropriate level than it was a year ago.

European Central Bank

Wunsch (Neutral). Weekend: We hiked 400 bps and we might have to do more, we have more ground to cover, real rates are still quite low, if fiscal policy remains supportive then monetary policy will have to do more to get inflation under control.

De Cos (Dove). Mon: Policy tightening is well underway but based on the information currently available to us we have some way to go, interest rates will have to remain in restrictive territory for an extended period of time.

Simkus (Hawk). Tue: Expects a 25 bps rate hike in June and July, September is too early to say.

Centeno. Wed: Spain's CPI reading shows that Europe's inflation is easing, doesn't see a risk of monetary policy overshooting, reversal of supply shock should slow inflation.

Villeroy (Neutral). Wed: It is quite likely that inflation has passed its peak in France, perseverance counts for more than speed regarding monetary policy, will bring inflation down to 2% between now and 2025, markets are absorbing QT smoothly and positively. Thu: Upcoming rate hikes will be marginal, rate hikes are beginning to have an impact on inflation, we will bring inflation back to 2% by 2025.

De Guindos (Dove). Wed: Inflation data today and yesterday has been positive, victory over inflation is not there yet but the trajectory is correct. Thu: A big part of our journey to raise rates has been done but there is still some way to go, recent inflation data are positive but still far from target.

Müller (Hawk). Wed: Very likely that we will hike by 25 bps more than once, probably too optimistic to see rate cuts in early 2024, core inflation shows no signs of slowing yet.

Visco (Dove). Wed: Must proceed with the correct degree of graduality now that rates are in restrictive territory, longer-term inflation expectations remain in line with the definition of price stability.

Kazaks (Hawk). Thu: It is hard to say where interest rates will peak but rates will stay at their peak for a while.

Rehn (Neutral). Thu: The monetary policy journey is not over yet, core inflation must slow before mulling easing, the inflation outlook continues to be too high for too long, a lasting rise in inflation expectations is an upside risk to inflation, the lags and the strength of policy transmission to the real economy remain uncertain.

Lagarde (Dove). Thu: We need to continue with rate hikes until we are sufficiently confident that inflation is on track to return to 2% in a timely manner, we cannot say that we are satisfied with the inflation outlook, a period of catch-up wage growth need not cause unduly persistent inflation over time, rate hikes are already feeding forcefully into bank lending conditions.

Panetta (Neutral). Fri: We have not reached the end of the rate hike cycle but we aren't far away from it, inflation is too high but there is no reason to worry, now is not the time to be too hasty raising rates, the debate will soon shift from level of interest rates to that of maintaining them over time, cannot rule out a technical recession in the Eurozone, committed to getting inflation back to 2% target.

Vasle. Fri: More rate hikes needed to get inflation to 2% target, core inflation remains high and persistent.

Makhlouf. Fri: Likely to see another rate hike at the next meeting, beyond probable hikes in June and July the picture is a lot less clear, inflation fall is very welcome but not definitive and underlying pressures are still quite strong.

Bank of England

Mann (Hawk). Wed: The gap between UK headline and core inflation is more persistent than in the US and the Eurozone, in core we do start to see implications coming through pricing channels and wage negotiations into something that is persistent.

Reserve Bank of Australia

Lowe. Wed: Monetary policy is in restrictive territory, the RBA is in data-dependent mode, wage growth has not been a source of inflation, there is not a single variable that drives RBA policy decisions, one factor behind May rate increase was to reinforce the RBA is serious about getting inflation down, inflation expectations are well anchored and we can't take this for granted, the RBA is serious about the inflation target but also want to preserve labour market gains, mid-2025 is pressing the length of time we can reasonably take to achieve the inflation target, the risk to inflation is to the upside and we need to be attentive to that.

Swiss National Bank

Jordan. Wed: We need to bring inflation below 2% as soon as possible, the longer inflation stays above 2% the harder it is to bring it down, sees inflation risks higher than deflation in the future due to deglobalisation, rising rates are positive for the banking system and will not damage financial stability in Switzerland, concerned about the speed and size of outflow of deposits.

Schlegel. Fri: Cannot rule out further monetary policy tightening, ready to be active in forex markets to ensure appropriate monetary conditions, cannot sound the all-clear on inflation despite recent dips in the data, inflationary pressure is broadening.

Bank of Japan

Ueda. Tue: We have not reached sustainable 2% inflation, will patiently maintain easy policy as there is still distance to go to stable 2% inflation, will continue bond buying operations, inflation will slow a great deal around the middle of FY 2023 and is likely to rebound after that but uncertainty is high. Wed: Whether inflation is caused by demand or supply has important implications for monetary policy decision making, increase in inflationary pressure has been cause by supply factors, recent global inflation has also been influenced by demand factors, it may be difficult to deny the possibility that we are already in a new normal that is different from the period of "low for long" inflation. Fri: Will maintain massive monetary easing as it will take more time to achieve our price target, buying of J-REITs is part of massive monetary easing, not the time to debate specific exit strategy including possible sale of J-REIT holdings, CPI likely to slow quite clearly in mid-to-later half of the current fiscal year, trend inflation likely to heighten ahead but will take time.

Kanda. Tue: Closely watching FX moves, will respond appropriately if necessary, not focussing on specific levels, important for currencies to move stably and reflect economic fundamentals, no intention for today's meeting to serve as a verbal intervention against Yen weakening.

Suzuki (FinMin). Fri: Exchange rates are driven by various factors, a weak Yen has various impact on Japan's economy such as exports and import prices.

Economic Data

Monday, 29.05.23

Tuesday, 30.05.23

Wednesday, 31.05.23

Thursday, 01.06.23

Friday, 02.06.23

Links to relevant central bank releases in previous editions of this newsletter:

Fed

FOMC Statements: 19/2023 | 13/2023 | 06/2023 | 50/2022 | 45/2022 | 39/2022 | 31/2022 FOMC Meeting Minutes: 22/2023 | 15/2023 | 09/2023 | 02/2023 | 47/2022 | 42/2022 | 34/2022 | 28/2022 | 25/2022 Crib Sheets: 05/2023 | 50/2022 | 37/2022

ECB

Rate Statements: 19/2023 | 12/2023 | 06/2023 | 50/2022 | 44/2022 | 37/2022 | 30/2022 Meeting Minutes: 17/2023 | 10/2023 | 04/2023 | 47/2022 | 35/2022 | 28/2022 | 21/2022 Economic Forecasts: 21/2022 Crib Sheets: 11/2023 | 05/2023 | 50/2022 | 43/2022 | 36/2022

BOE

Rate Statements: 20/2023 | 13/2023 | 06/2023 | 50/2022 | 45/2022 | 39/2022 | 32/2022 | 25/2022 Financial Stability Reports: 28/2022 Crib Sheets: 05/2023 | 50/2022 | 37/2022

RBA

Rate Statements: 19/2023 | 15/2023 | 11/2023 | 07/2023 | 50/2022 | 45/2022 | 41/2022 |37/2022 | 32/2022 | 28/2022 Meeting Minutes: 21/2023 | 17/2023 | 09/2023 | 51/2022 | 47/2022 | 43/2022 | 39/2022 | 34/2022 | 30/2022 | 26/2022 | 21/2022 Statements on Monetary Policy: 19/2023 | 07/2023 | 45/2022 | 32/2022 Crib Sheets: 40/2022 Financial Stability Reports: 41/2022

RBNZ

Rate Statements: 22/2023 | 15/2023 | 09/2023 | 47/2022 | 41/2022 | 34/2022 Meeting Minutes: 07/2023 Crib Sheets: 40/2022

BOC

Rate Statements: 15/2023 | 11/2023 | 05/2023 | 50/2022 | 44/2022 | 37/2022 Crib Sheets: 43/2022 | 36/2022 Summary of Deliberations: 18/2023

SNB

Rate Statements: 13/2023 | 50/2022 | 44/2022 | 39/2022 | 25/2022 Crib Sheets: 50/2022 | 37/2022

BOJ

Rate Statements: 18/2023 | 11/2023 | 04/2023 | 51/2022 | 39/2022 | 30/2022 | 25/2022 Summary of Opinions: 20/2023 | 13/2023 | 05/2023 | 52/2022 | 46/2022 | 41/2022 | 31/2022 Crib Sheets: 43/2022

Photo Credit: Midjourney with the prompt: Bull rider

What happened to the currency bullish/bearish bias on the Playbook for the week? I have family and kids to feed, I neeeeeed this! 😩 (just kidding)

Always a great macro digest