Outlook for Week 08/2023

Looking back on quite a few central bank speakers this week...

This is going to be a short version of the newsletter without the Analysis section. I've updated the Summary table with what I saw when I went through all the charts.

Welcome to issue #43 of fx:macro!

This newsletter is quite long, so there's a Summary section at the top. Everything you find there is derived from data and news I show in detail in the second and third parts of the newsletter (Week in Review and Market Analysis). I encourage you to go through those parts because they are basically the reasoning behind the conclusions I present in the Summary.

If you're using Gmail, you will need to click “View entire message” at the bottom since it can't display the whole thing.

The cover image is AI-generated via DALL-E 2. If you want to guess the prompt, I put it at the end of the newsletter.

If you like this newsletter, please consider subscribing and sharing it or forwarding it to others who might be interested. I'm also on Twitter @fxmacroguy if you want to reach out.

Before we dive in, I'd like to introduce you to one of my favourite must-read newsletters:

Table of Contents

Summary (Playbook, Calendar,

Levels, FX Drivers, Downloads)Week in Review: a) Central Banks, b) Economic Data

Market Analysis: a) Growth and Inflation, b) Yields, c) Central Banks and the US Dollar, d) Sectors and Flows, e) Sentiment and Positioning, f) Market Risks, g) VariousTop 3 Macro Charts of the Week

Summary

Playbook for next week

This is the shortest possible summary of everything you will find in the rest of this newsletter.

Economic Calendar for next week

Currency Drivers

For an explanation check out this link.

Downloads and Links

Difftext of the Summary from last week: link to diffchecker.com

Central bank speaker recap for the week:

Week in Review

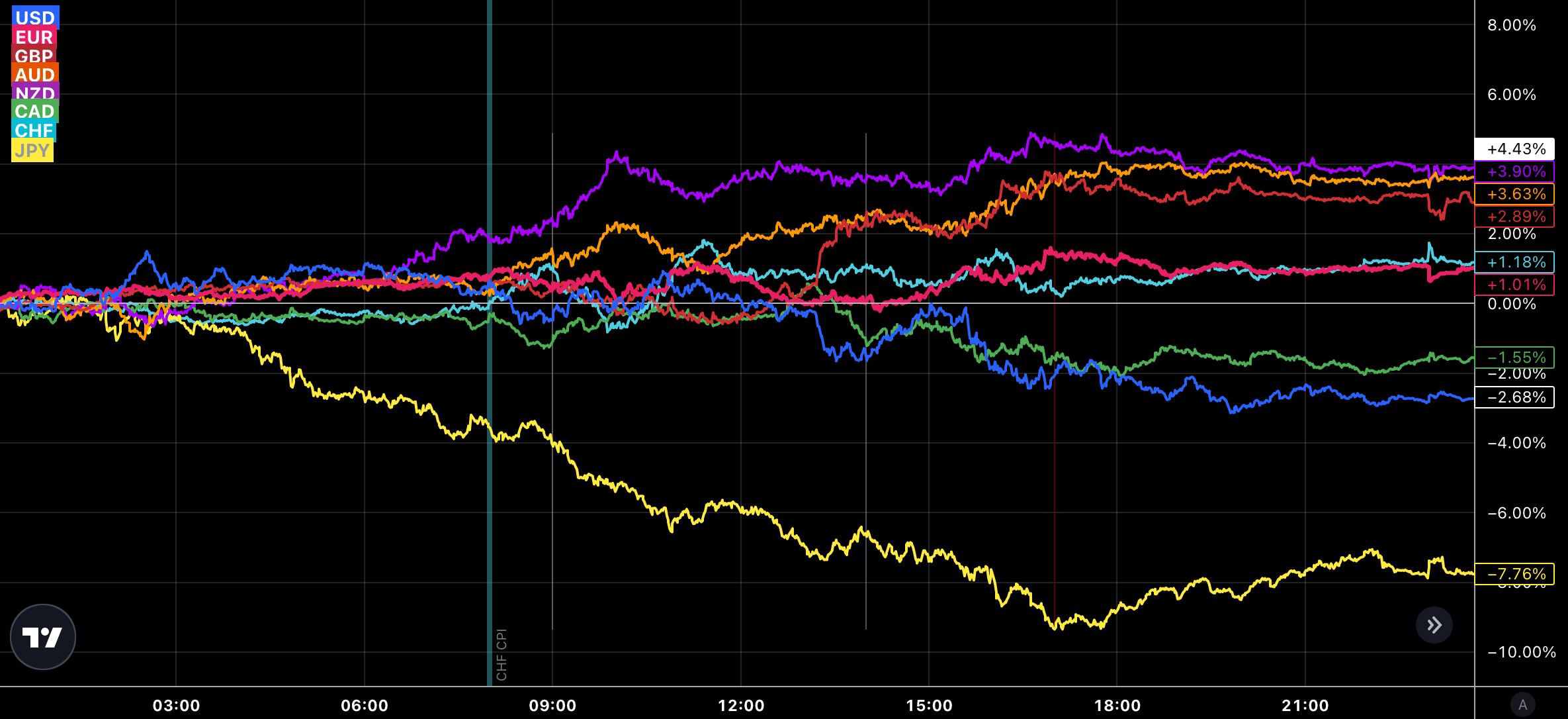

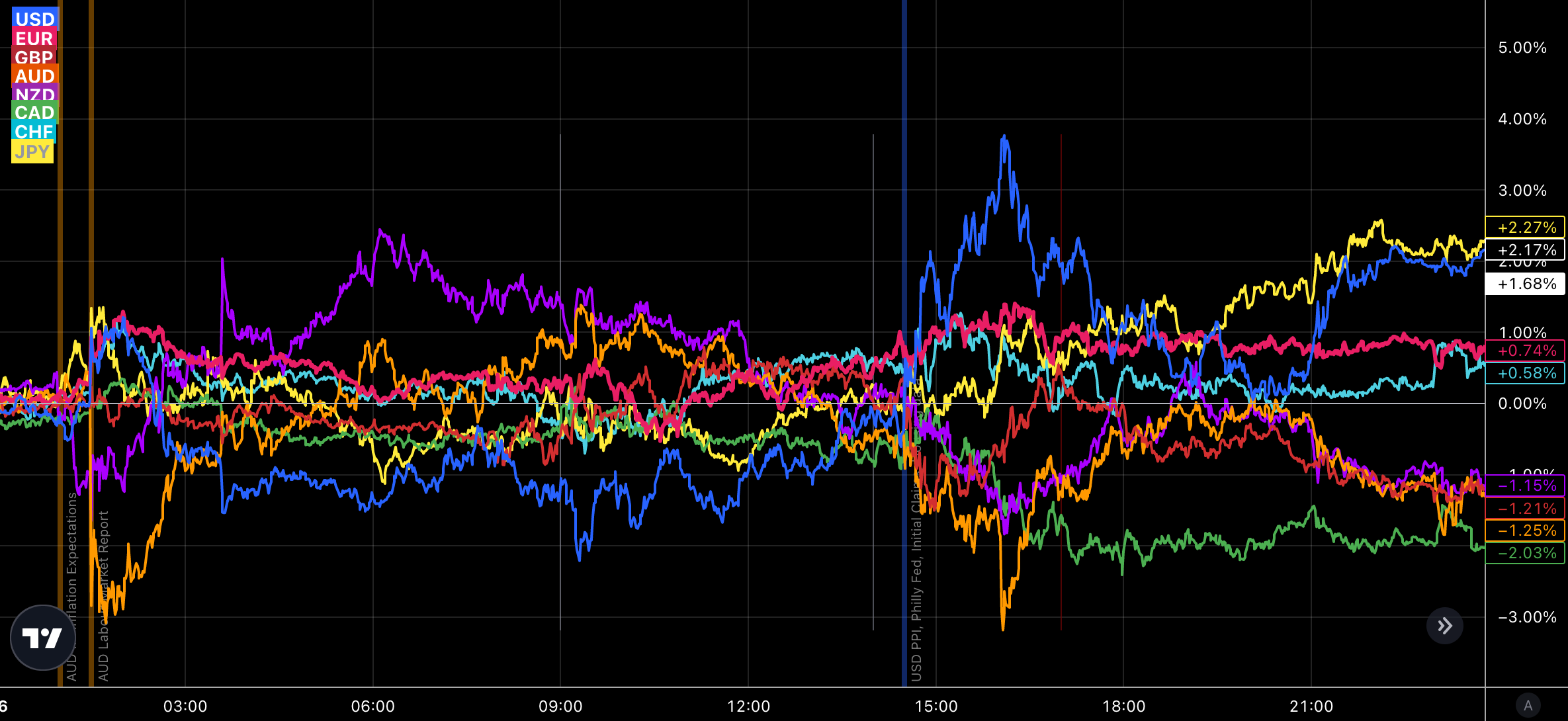

Central Banks

Confab, Speakers, News

Federal Reserve

Bowman (Neutral). Mon: We expect to continue raising rates, not seeing as much moderation in inflation as we would like, there is a lot of data between now and the next FOMC meeting. Fri: We need to raise rates until we reach a sufficiently restrictive level, recent data indicates we have yet to be restrictive, not seeing what we need to see on inflation, numbers are jumping around a bit, thought the data before the last meeting showed a moderation in inflation but most recent data "has been surprising", wants to see a consistent decline in inflation, it's a long way to get inflation back to goal.

Barkin (Neutral). Tue: There's going to be a lot more inertia and persistence in inflation than we want, nobody knows how inflation will play out this year or next, will be data-dependent, may or may not take rates higher if inflation persists, very good case for leaving rates higher for longer for a period of time, the risk of doing too much is outweighed by the risk of doing too little, we might not go as far on the rate peak if inflation settles. Fri: 25 bps rate path offers flexibility to respond to data, more rate increases required to control inflation, "we will have to see" how many rate hikes, seeing some progress on inflation with demand normalizing, not taking signal from jobs and retail sales due to seasonal adjustments,

Logan (Neutral). Tue: Must be prepared to keep raising rates longer than anticipated if needed, need continued gradual rate hikes until we see convincing evidence inflation is falling to 2% in a sustainable and timely way, top risk is tightening policy too little, should not lock in a peak policy rate or precise path, little sign of improvement in core services ex housing inflation, number one priority is to restore price stability.

Harker (Neutral). Tue: Thinks we need to continue in 25 bps increments above 5% for a while, how much above 5% we need to go depends on incoming data, expects policy rate to be restrictive enough to hold rates in place at some point this year, we are not done yet but likely close, today's inflation report shows inflation isn't moving down quickly.

Williams (Neutral). Tue: Outlook for year-end FFR at 5.00-5.50% looks reasonable, recent data supports the case for more rate rises, have not yet gotten rates to where they need to be, there is a risk inflation stays higher than expected, will need restrictive levels for some time, possible the Fed cuts rates in 2024/25 to reflect lower inflation, will take several years to get inflation back to 2%, jobs market is extremely tight and wages gains elevated.

Mester (Hawk). Thu: Not ready to say whether Fed needs bigger rate rise at next FOMC meeting, need to get above 5% and stay there for a while, more upside inflation surprises could make policy more aggressive, doubts the need to cut rates later this year, can't be complacent about getting inflation back to target, Fed has more work to do on inflation, saw a compelling case for 50 bps at the last meeting, bigger risk is to undershoot in effort to control inflation, a recession wouldn't be a positive outcome but it may happen, hasn't pencilled in a recession.

Bullard (Hawk). Thu: Sees policy rate of 5.25-5.50% as appropriate, wouldn't rule out anything at the next Fed meeting, advocated for 50 bps at the last meeting to get adequately restrictive, if the Fed can't control inflation soon it risks a replay of the 1970s, continued rate increases would lock in slowing inflation, sceptical labour market will cool as much as some expect but inflation can still fall.

European Central Bank

Visco (Dove). Sun: Must avoid unnecessary and excessive rise in real interest rates given the levels of public and private debt, rates must continue to rise in a progressive and measured way on the basis of incoming data.

De Guindos (Dove). Mon: Rate increases beyond March will be data-dependent, the ECB now is a bit more positive on the economic outlook.

Centeno. Mon: Smaller rate hikes need mid-term inflation nearing 2%, inflation surprised the ECB to the downside, March forecasts will be very important in defining the terminal rate. Tue: Full impact of rate hikes may not reach the economy.

Makhlouf. Tue: ECB could raise rates above 3.5% and hold them there, open to acting forcefully to get inflation down to 2% target, rate cuts in 2023 are unlikely.

De Cos (Dove). Wed: Recent inflation data have been somewhat encouraging, data points to inflation falling more strongly in the coming months than anticipated in December, withdrawal of fiscal support measures could make inflation more persistent.

Lagarde (Dove). Wed: Long-term inflation expectations warrant monitoring even though they are near 2%, price pressures remain strong and inflation is still high, risks to the growth outlook are now balanced, risks to inflation have also become more balanced, wages are growing faster supported by robust employment prospects.

Ulbrich. Wed: Bundesbank Chief Economist. We will see very strong declines in housing construction market investment this year, there is a bit of a perfect storm coming together with rising interest rates, declining disposable income, higher inflation and energy prices.

Panetta. Thu: ECB should not unconditionally pre-commit to future policy moves, extent and duration of monetary policy matter now that rates are in restrictive territory, must now consider risks of overtightening, smaller rate hikes can ensure better calibration of policy, wages are an upside risk, headline inflation may fall below 3% towards the end of the year, core inflation cannot turn on a dime but will eventually follow headline inflation.

Lane. Thu: Much of the ultimate inflation impact of our measures is still in the pipeline, open-minded about precise scale of monetary policy tightening that will be needed, ECB will have data-dependent meeting-by-meeting approach to setting interest rates, significant amount of excess savings could dampen the transmission of higher policy rates to the economy and inflation.

Stournas. Thu: Interest rates may not need to be increased to a level that could lead the Eurozone to a hard landing, data point to easing inflation pressures and modest expansion in economic activity.

Schnabel (Neutral). Fri: A 50 bps rate hike in March is needed under all scenarios, isn't easy to say if ECB policy is already restrictive, sees risk that markets are underestimating inflation, still far away from claiming victory in inflation battle, broad disinflation process has not yet started.

Villeroy (Neutral). Fri: Sees rates peaking this summer which technically ends in September, will probably go above 3% after March, how long rates are kept at the terminal rate is key, timing of rate cuts "surely" isn't a question for this year, central question for rate cuts is the return of inflation outlook to 2% target, inflation is possibly persistent, inflation rate may half by the middle of the year.

Bank of England

Haskel (Hawk). Mon: You want to be "really, really careful" on inflation, would prefer to make policy with much more attention on the data flow over the next few months.

Pill. Thu: Labour market remains tight in an absolute sense, Tuesday's labour market report pointed to sings that the jobs market loosened a little in line with MPC narrative.

Reserve Bank of Australia

Lowe. Wed: Not at peak for rates yet, unsure how high rates have to go, there is a risk we haven't raised rates enough and that we have tightened policy too much, monetary policy is restrictive, government fiscal policy is broadly neutral. Fri: Expects further rate hikes will be needed over the months ahead, not finished on rate hikes yet, moving in little increments rather than large ones is preferable, how much rates have to rise depends on the global economy, inflation, the labour market and household spending; one risk is not doing enough and the other risk is that we move too fast or too far, monetary policy is restrictive, fiscal policy is neutral, it takes 18-24 months for the effects of rate hikes to be felt in the economy, rates could come down next year if we get on top of inflation but a few things would have to go right. Trimmed mean CPI of 6.9% vs. 6.5% forecast is a significant difference, inflation expectations remain well anchored, impact of higher rates is being felt very unevenly across the community, pool of savings is substantial, the labour market remains extremely tight, hearing that salary growth has accelerated, last two months' jobs are difficult to assess due to seasonality, if we saw another weak jobs report we might reconsider tight labour market.

Ellis. Fri: Labour market is a little less tight than a few months ago, exceptionally large number of people awaiting new jobs.

Jones. Fri: Relatively small number of loans are now in negative equity, some resiliency in household balance sheets.

Bank of Canada

Beaudry. Thu: Important to stay the course in the fight against inflation despite short-term pain caused by high interest rates, Canadians shouldn't be concerned if we follow a slightly different path than other central banks, it will take time to get back to 2% inflation target.

Bank of Japan

Matsuno. Tue: Monetary policy is up to the BOJ to decide, Ueda is an internationally prominent economist and well-versed in financial policy. Thu: BOJ has jurisdiction over monetary policy, government and the BOJ will guide policy to achieve structural wage rise and stable and sustained achievement of price target.

Kishida. Wed: Kazuo Ueda is the best fit to lead the central bank, he is a well-known economist globally, appointment was made after taking market impact as well as economic and wage growth and price stability targets into consideration.

Uchida. Fri: BOJ has decided to launch a pilot program on CBDC this April, aim is to test technical feasibility and utilize skills and insights of private businesses.

Economic Data

Monday, 13.02.23

Tuesday, 14.02.23

Wednesday, 15.02.23

Thursday, 16.02.23

Friday, 17.02.23

Links to relevant central bank releases in previous editions of this newsletter:

Fed

FOMC Statements: 06/2023 | 50/2022 | 45/2022 | 39/2022 | 31/2022 FOMC Meeting Minutes: 02/2023 | 47/2022 | 42/2022 | 34/2022 | 28/2022 | 25/2022 Crib Sheets: 05/2023 | 50/2022 | 37/2022

ECB

Rate Statements: 06/2023 | 50/2022 | 44/2022 | 37/2022 | 30/2022 Meeting Minutes: 04/2023 | 47/2022 | 35/2022 | 28/2022 | 21/2022 Economic Forecasts: 21/2022 Crib Sheets: 05/2023 | 50/2022 | 43/2022 | 36/2022

BOE

Rate Statements: 06/2023 | 50/2022 | 45/2022 | 39/2022 | 32/2022 | 25/2022 Financial Stability Reports: 28/2022 Crib Sheets: 05/2023 | 50/2022 | 37/2022

RBA

Rate Statements: 07/2023 | 50/2022 | 45/2022 | 41/2022 |37/2022 | 32/2022 | 28/2022 Meeting Minutes: 51/2022 | 47/2022 | 43/2022 | 39/2022 | 34/2022 | 30/2022 | 26/2022 | 21/2022 Statements on Monetary Policy: 07/2023 | 45/2022 | 32/2022 Crib Sheets: 40/2022 Financial Stability Reports: 41/2022

RBNZ

Rate Statements: 47/2022 | 41/2022 | 34/2022 Meeting Minutes: 07/2023 Crib Sheets: 40/2022

BOC

Rate Statements: 05/2023 | 50/2022 | 44/2022 | 37/2022 Crib Sheets: 43/2022 | 36/2022

SNB

Rate Statements: 50/2022 | 44/2022 | 39/2022 | 25/2022 Crib Sheets: 50/2022 | 37/2022

BOJ

Rate Statements: 04/2023 | 51/2022 | 39/2022 | 30/2022 | 25/2022 Summary of Opinions: 05/2023 | 52/2022 | 46/2022 | 41/2022 | 31/2022 Crib Sheets: 43/2022

Photo Credit: DALL-E 2 with the prompt: Trading on the beach is harder than it looks.

Great breakdown as always. Much Appreciated!

I do have a question. maybe I missed something on the Swiss CPI but I was seeing MoM increase 0.6 expected 0.4(Trading economics) and 0.6 increase vs expected at 0.5%(Forex Factory)

YoY CPI also increased 3.3% vs 2.9% (Trading economics). Wouldn't that be a upside surprise and inflationary still.

great take, thank you!