[FREE] fx:macro Lite / 12.11.23

Of economists and fantastic beasts

Hi there! It's already Sunday, so it's time for another edition of fx:macro Lite! Great to have you here!

This week, we'll look at one of my favourite indicators: the Citi Economic Surprise Index. And when I asked MidJourney for an image of economists all running in a herd (because that's one thing this indicator captures), I got this delightfully weird set of suggestions…

Let's get started…

In case you missed the usual deep-dive yesterday, you can still sign up for that here and get access to the premium content:

💎 Central Bank Overview

We had the RBA meeting this week, the RBA's projections, the BOC's Summary of Deliberations and the BOJ's Summary of Opinions this week. Here's the central bank overview sheet I'm using that puts everything you need to know about the recent G8 central bank meetings in one place: rates, statements, press conferences, projections, minutes:

💡 The Citi Economic Surprise Index

I first read about the CESI in a book called The Global Macro Edge by John Netto. The book comprises sections from different authors, most of which I had never heard of (and still don't know much about…). In Chapter 4, Jason Roney gives a brief overview of his quantitative macro approach. He's heavily relying on the CESI to gauge how different economies are performing. Here's a quote from the book:

The second factor I use to get a sense of the data trend is the set of surprise indexes. This helps contextualize how a market may react to any given news flow. The market may be at -20 on the surprise index irrespective of whether the unemployment rate is at 10 percent or 5 percent. These surprise indexes do a great job showing the recent trend of market surprises or disappointments.

Specifically, I use the set of Citigroup surprise indexes to track this second component, which one can get for different regions of the world (US, Europe, Asia, South America). One of the reasons I use these particular metrics can be seen if you overlay a very basic three-period moving average and ten-period moving average on any of these charts. When the shorter term three-period moving average is above the ten-period moving average, it’s a pretty safe bet that most money managers will have to be long those markets. However, this is obviously not an end-all-be-all strategy—when economic times are good, it is very hard for managers to not justify being fully invested.

The Citi Surprise Indexes in and of themselves, are not something I can trade as a standalone indicator. However, they do a good job of providing a framework to understand the trend of any given region. They reflect how an economy is performing relative to expectations, where a positive reading means data releases have been stronger than expected, and vice versa.

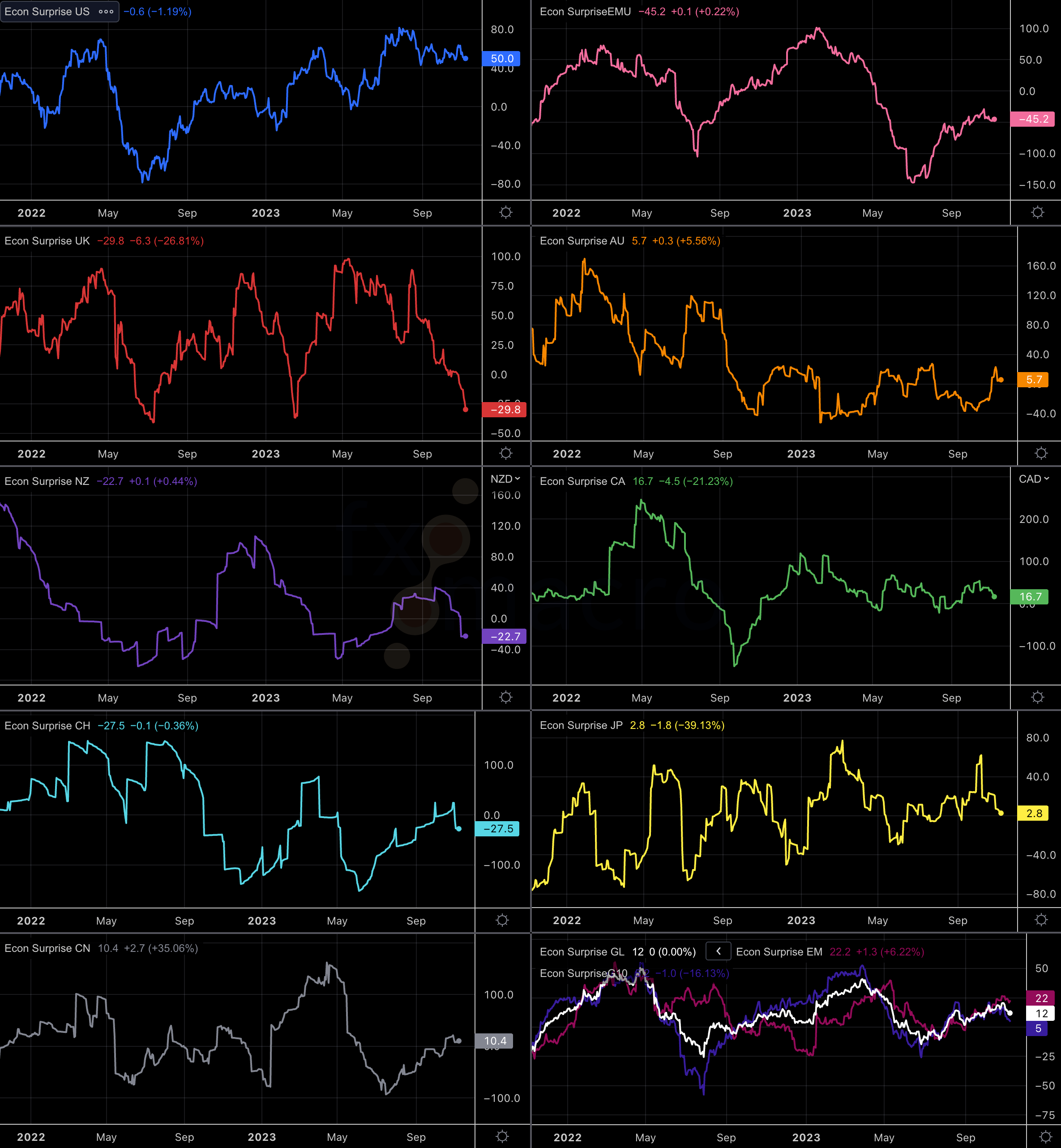

Unfortunately, the Surprise Indexes aren't available for free but they are on Bloomberg (of course…) and Reuters. The following chart shows what it looks like for the US over 20 years or so:

The basic idea is that a reading above zero means that economic data is coming in stronger than expectations, while prints below zero (unsurprisingly…) mean it comes in worse than expectations. In practice, a rising CESI is bullish and a falling one is bearish.

I've bolded the “stronger/worse than expectations” because that's really the key: most of the time, we're not trading absolute levels of data but whether it comes in better or worse than what's expected (and therefore, presumably, what's priced in). That's also why the CESI isn't saying whether the economy is doing well or badly: it's just doing better or worse than expectations.

How are “expectations” defined in that context? They are the consensus estimate of economists, their mean or median. That brings us to a well-known phenomenon called “herding” or groupthink. Here's what Brave's new AI has to say about it:

“Herding” refers to the phenomenon where many economists make similar predictions or forecasts, often based on the same set of assumptions or factors, rather than independently analyzing the data and coming to their own conclusions. This can lead to a groupthink effect, where the majority view becomes the dominant view, even if it's not necessarily the most accurate one.

Think about it this way: you're an economist with a wife, an ex-wife, three kids in college and a golf club membership to support. You think GDP will print at 5% this quarter but everyone else at lunch tells you they think it's going to be about 2%. What do you do? If you care about your career, you're going to say: 2.3% or something but definitely not the 5% you really believe. Why? Because there's just no upside to placing your bet far away from everyone else: if you're spot on with your 5% you'd get the maximum amount of praise, fame or whatever it is economists get. But: you'd get basically the same hero treatment if you're far off from the actual print but still the most bullish forecaster because “nobody imagined it could be 5%”. But consider the downside: if you're the most bullish forecaster with your bet far away from everyone else and you're wrong then everybody (including your boss) is going to think you're completely nuts. Not a good outcome, and not a good career booster.

Back to the CESI: herding is one part of why it exists and why it behaves the way it does. Look at the COVID spike as an example: expectations were abysmal in April of 2020 but then CESI shot up and reached a high in July. That's the textbook example of everyone (and their forecasting models) being caught on the wrong foot because expectations and reality were just so much out of sync. You know what happened in markets…

The interesting thing is that it's a mean reverting index: forecasters adjust their models and anchors, and then it goes the other way. That's why an extreme reading on either side can well be the peak for optimism or pessimism around an economy.

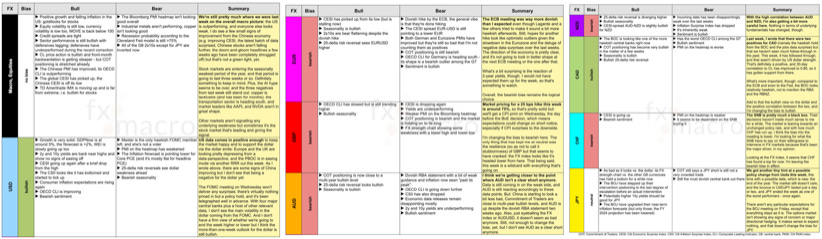

Since CESI is available for every major economy, it's a great tool for currency traders. You might know that chart from my weekly outlook:

The CESI for the UK (left column, second from the top) has dropped quite sharply from highs to close to lows in a couple of months. That's bearish because the reality of the UK economy has underperformed what was priced in. But: we're close to extreme levels where expectations are so bad that things can only get better. At Hogwarts, the UK economy would be graded P (as in Poor) or D (as in Dreadful) but it might soon become E (for Exceeds Expectations), which is still not an O (for Outstanding).

One last thing I want to mention is that you can build spreads with CESIs from different countries and overlay them on currency pairs. It works quite well with AUD/NZD for example. The purple line is the Aussie CESI minus the Kiwi one. It's often enough telling you where the currency pair should go:

That's it for this week, let me know what you think!

Until next weekend

FXMG

Excellent presentation of how to use these surprises. Effectively, they give a clear indication of how people HAVE been positioned- but in a different way than the CoTs...