Podcast Write-up: The Macro Trading Floor w/ Nick Stadtmiller

Some interesting takes on Emerging Markets

Welcome to another issue of Wednesday's podcast write-ups, this time with the latest episode of The Macro Trading Floor.

In case you've missed it, here's a link to my usual weekend piece with a recap of the relevant macro events and a comprehensive look at markets from every different angle:

If you like this newsletter, please consider subscribing and sharing it or forwarding it to others who might be interested. I'm also on Twitter @fxmacroguy if you want to reach out.

One more thing. You seem to like newsletters, so here's a great way to discover new stuff to read for free: The Sample. They will regularly send you an issue of a different semi-random newsletter you might be interested in. If you sign up using my referral link, I get bonus points and my newsletter will be forwarded to others to check out.

Release date: 14.08.2022

Host(s): Alfonso Peccatiello, Andreas Steno

Guest(s): Nick Stadtmiller (@NickStadtmiller)

Charts in the Intro section have been taken from the podcast video. Charts in the other sections have been added by me.

Notes

Intro

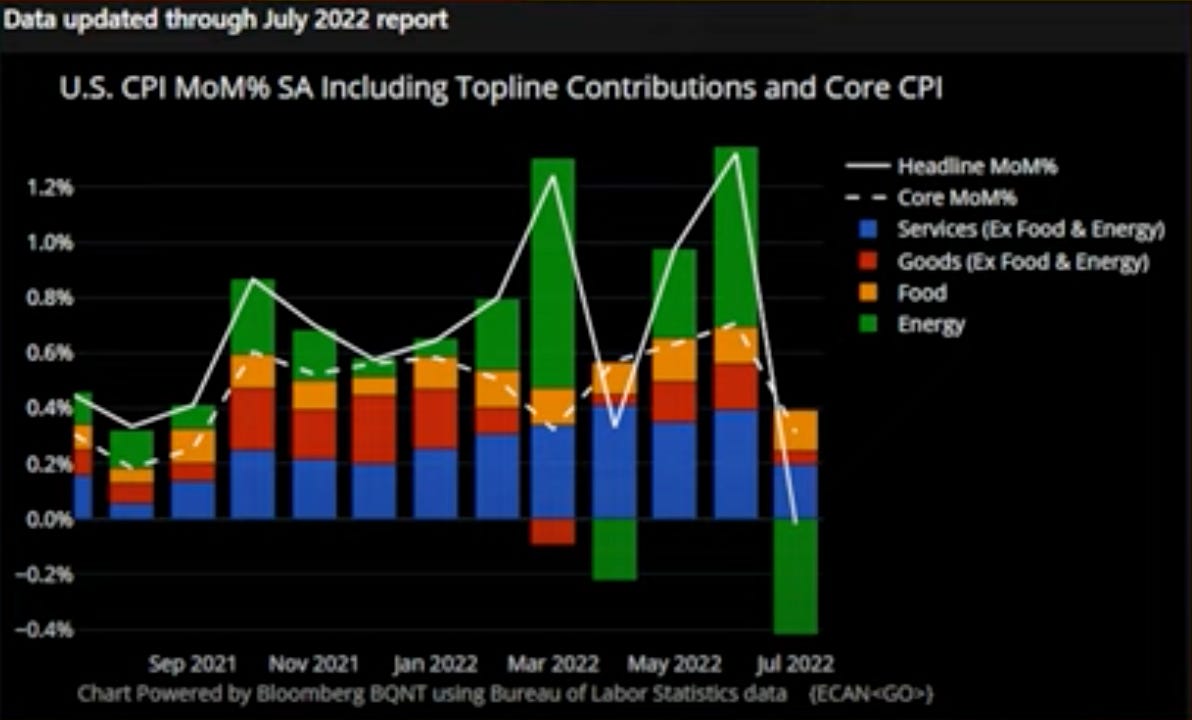

Alf mentions the CPI prints from last week that was a lot lower than expectations. Andreas thinks this could be a short-term turning point in the market cycle: if the market senses a change of trend it starts to price it in.

Andreas looks at NFIB Price Plans from this week that has turned lower as well. He feels confident that the peak in inflation is in now.

Alf mentions that the composition of inflation is also a lot more friendly to policymakers, and if you combine it with the labour market report the week before, the market might price in a goldilocks scenario. Markets are probabilistic, so they don't price final outcomes, and now a soft landing seems a lot more achievable. He wants to know if Andreas would go for a goldilocks asset allocation now.

Andreas thinks it's too early: once the inflation peak is in, it's a decent time to buy risk assets, but this time it's different because the growth cycle is falling apart. Commodities are still driving inflation, and the commodity market is telling us growth is slowing. So, it's not a very good time to load up on risk now. He wants the Fed to at least admit that growth is slowing down hard.

Alf points out that bond markets and OIS are still pricing that the tightening cycle will stop early next year, and that pricing has been historically been right:

The Fed pivot this time is a lot more complicated because of high inflation, though.

Inflation in Europe is different than in the US because the electricity situation is a lot worse in Europe with forward electricity prices being significantly higher than spot. Andreas thinks the ECB might have to hike for longer than the Fed for that reason. The divergence between the US and the European yield curve could be “almost a bargain trade”. Alf translates it as: Eurodollar SOFR Z22/Z23 boxed against Euribor Z22/Z23.

Alf thinks everybody has forgotten about QT. The asset side of the balance sheet is easy to understand: the Fed stops reinvesting in treasuries. But the liability side of the balance sheet has to shrink as well: the most aggressive way to do that is to reduce bank reserves. The liability side is made up of a lot of reverse repos and TGA (Treasury General Account). Alf expects bank reserves to tumble as a result of QT.

Andreas thinks crypto is the perfect hedge against the balance sheet size of the Fed, but not a good hedge against inflation as in CPI. He thinks right now is a window of opportunity for crypto, but the true opportunity for crypto and long-duration tech stocks will be when the liquidity cycle turns around again.

Andreas segues over to Emerging Markets: the BRL has rebounded and MXN is moving as well.

Feature Interview

Nick Stadtmiller is the Director of Emerging Markets Strategy at Medley Global Advisors.

Andreas: What do you think about current sentiment and a potential soft landing?

Nick thinks there's a lot of uncertainty and there are a lot of diverging opinions out there. He thinks that there's going to be a severe recession in Europe, but the uncertainty for the US economy is very high. That and the strong dollar hurt sentiment around emerging markets.

Alf: Inflation in the US has slowed down this week. How does it influence your thought process?

Nick responds that the sell-off in the dollar and the yield curve steepening were a goldilocks moment for emerging markets. The market expects the Fed to hike less while at the same time the 10-year yield isn't coming down as it would in a global growth slowdown. It also takes pressure off EM central banks if the Fed stops hiking: widening yield differentials would force them to hike even if they see a recession in the future. Still, he doesn't believe we're there yet, because we don't know how sticky inflation will be, and he thinks the market might be a little too optimistic on that front.

Andreas: Is it possible to kill the current inflation momentum without causing a recession in the US?

A soft landing is very hard to achieve because so many things have to go perfectly. It would be too difficult for the Fed to let inflation remain above target in sacrifice of the employment mandate. Nick expects that the Fed will have to accept higher unemployment and lower growth to achieve its inflation goal.

Alf: What's your view on the dollar and how does it tie into the emerging market economies?

Usually, people use the Dollar Index (DXY) as a proxy, which is about 60% EURUSD. But even EURUSD is very highly correlated to EM currencies. Currently, the market isn't pricing an aggressive and sustained interest rate path that the Fed has set out. So, Nick believes there could be an upside to the dollar that puts pressure on EM central banks to be more hawkish than they planned because they face persistent currency weakness over the next several months.

Andreas: Which countries will be the relative winners and losers in a scenario like this?

Nick points out there's a lot of uncertainty about his hypothesis of a stronger dollar. He can see the dollar pulling back and yields coming down significantly, so he believes it's very hard to make directional bets on single EM currencies. Rather, he favours looking for relative winners. He looks for countries with stronger domestic fundamentals: Mexico can outperform in Latin America, particularly over Brazil, since it's closely tied to the US economy.

Alf: What's your take on Europe?

Russia and Ukraine are obviously knocked out. Turkiye is a complete mess, but Nick expects them to “muddle through without a serious crisis over the next year”. The CE3 countries (Poland, Czech, Hungary) have interesting monetary policy stories.

Those countries hadn't moved rates for years and had very dovish forward guidance in effect:

The Czech central bank went from being the most hawkish one to being pretty much the most dovish bank

Hungary has the lowest inflation but by far the highest policy rate and they give hawkish guidance

Hungary has the weakest fiscal position, and there's a lot of hope for EU funds while PM Orban cosying up to Russia and spitting in the EU's face is a risk. So, the market may be too optimistic about the recovery fund money. Also, Hungary is much more dependent on gas than Poland and Czechia, especially since they depend heavily on Russian gas, which can only get into Hungary through either the EU or Ukraine. That makes them potentially much more vulnerable. Nick thinks there's no way the rest of the EU will watch Hungary get away with sourcing cheap gas from Russia while Germany and other EU countries get cut off. So, it's a no-win situation for Orban, and Nick expects the Hungarian Forint to underperform among the CE3.

Andreas: It looks like Italians are exporting stuff to Turkiye, and from there to Russia. Are certain EU countries using this loophole to circumvent sanctions on Russia?

Nick has looked at the data in more detail, and he doesn't think it's a big issue but more of a catch-up from a dip around Covid. Italian exports to Turkiye are picking up, but global imports in Turkiye are picking up because of their reckless monetary policy. And Russian imports from Turkiye are probably substitution for goods they can't get elsewhere.

Alf: What's your take on China?

Zero-Covid has been the biggest headwind sentiment-wise, and there hasn't been a lot of willingness to provide a lot of monetary stimulus. The Chinese don't want total credit growth to run away again and have people accumulate bad assets, especially when you look at their problems with the real estate market. They are doing some infrastructure spending, and they've upped the percentage of stimulus that has to be spent on wages from 30% to 50%. It's more geared towards stimulating domestic demand vs. stimulating demand for importing commodities.

There's not going to be runaway growth with this kind of stimulus but more of a slow recovery back to a 5-5.5% growth range. Even if it's slow for China, compared to the rest of the world in a slowdown it's still pretty good.

A lot of Emerging Market policymakers are probably using models with data like Chinese GDP, industrial production and demand for commodities, so there's room for disappointment there. So, the current recovery in China probably doesn't have as much impact on other EMs as it did in the past.

Andreas: Do you fear China will become as uninvestable as Russia as tensions around Taiwan increase?

Nick says he's not an expert on that, but he's talked to a lot of them, and his opinion is basically a summary of what he's heard so far. He does not think it's a 6-month to 2-year risk, but on a longer timeframe it's on the horizon. A lot of investors worry about the risk since the Russian invasion of Ukraine, so it's going to keep a lot of capital from flowing into China.

Alf: Let's talk about India.

Southeast Asia is probably going to be a bright spot going into next year. Growth forecasts show accelerating growth, so the macro backdrop is more supportive than in EMEA or Latin America.

Andreas: Why do you like the outlook for Mexico more than for Brazil, as you mentioned earlier?

The tight labour market in the US leads to higher remittances for Mexico, which is a big source of foreign income. Import demand from the US is strong, too. There has also been quite a lot of fiscal responsibility, which is a surprise given the long-standing fears with AMLO as their left-wing president. The one risk factor is trade disputes with the US.

As for Brazil, lots of things have been going wrong for them lately: commodities are down, which is dragging their terms of trade lower and that's weighing on the Real. Also, Bolsonaro has engaged in a lot of fiscal spending to secure his reelection. Now it looks like his opponent, Lula, is going to win the election in October. He could well be more irresponsible than everyone expects already. But even if he's not, just normalizing fiscal policy and debt sustainability are going to be hard.

Alf: What is your actionable macro trade?

Number one is going long the PLN vs. the HUF as a geopolitical play:

Hungary's relationship with the EU isn't going to become any better, they're not going to get the EU recovery funds

Fiscal challenges in Hungary

Poland has a higher reliance on domestic demand (among others from the inflow of Ukrainian refugees)

Andreas: What do you think about the carry in that trade and in BRL vs. MXN?

Both of them are negative carry, PLNHUF is about -3% and MXNBRL is about -4.5%. Nick has a relatively short horizon on his trades, both trades could play out in the next few months.

Brazil is probably done hiking, whereas Mexico could even do 200 bps more, so the carry is likely to shrink. Poland doesn't have much room for disappointment, because its central bank is hawkish and they've said that they're going to hike more if inflation is sticky.

Post-interview discussion

Alf recaps that the two trades are:

long PLN vs. short HUF

long MXN vs. short BRL

Both of them have negative carry, and Andreas thinks that in the current environment he likes negative carry trades. The main reason for the PLNHUF trade is Victor Orban and his clash with the EU, especially when energy shortages increase. It's a geopolitical trade with a bit of mispriced interest rate differentials. As for MXNBRL, positioning in the Brazilian Real has been extremely positive and it's still positive despite the slide in commodity prices.

Andreas like both trades, but has concerns about timing and the fact that the global slowdown is currently not hard enough and more like a soft landing.

Alf says that the asset classes that are rallying now are associated with strong economic growth. Real interest rates are going up and equities keep on going. That means that either risk premia are compressed to pretty low levels because the Fed is managing the soft landing perfectly or economic growth will meaningfully surprise to the upside. So, you really need to get the story about the soft landing right.

Andreas says that it's usually a bad idea to bet against an inverted yield curve. And in about ten out of 13 attempts when the Fed tried to run a hiking cycle, it managed to hike the economy into a recession. He personally wouldn't bet on a soft landing.

Alf comes back to negative carry trades: they're not going to work when there are higher odds of a soft landing and implied volatility comes down across asset classes.

As for growth, Andreas says that we've had a technical recession in the US in H1. Nominal growth has been pretty strong, but it has been outrun by the high inflation numbers. For Q3 we could get a decent real growth print, because of inflation slowing while nominal growth remains relatively strong. He expects a drop in nominal growth significantly in Q4 regardless of inflation. He's therefore not believing in a soft landing, but for Q3 the market could rally because of growth outperforming inflation.

EPOL is an iShares ETF for Poland. Andreas thinks Poland is a high-beta play on the German economy as both countries are closely linked. If there's a small bullish surprise to the German outlook, it should perform well. He also doesn't think anyone is left to sell Europe, because everyone is bearish already, so he's slowly starting to become a bit more positive on Europe.