Podcast Write-Up: Options Insight Q3 Roundtable

Is the bottom in yet? No, no, no, no, "for me on an hourly basis"

Hi, welcome to the new Extras section of my newsletter. The main deal is still going to be the weekend FX and Macro update, but I wanted to add some more content that you might find useful:

The Extras section is going to feature about one email/post per week, usually around Wednesday.

The main idea is to always provide something that has value.

For now it's mostly going to be write-ups of finance and macro podcasts, but I might mix it up a bit later.

Why podcast write-ups? I listen to a ton of macro and finance podcasts. Some of them are pretty good, and I often take away a few things I hadn't thought about or considered before, especially when I disagree with what's being said. If the discussions or interviews get a bit more complex it's often hard to follow without pausing, rewinding and re-listening, though. And after the episode… most of what I just listened to is just gone, unfortunately. I tried taking notes a while ago and recently came across the idea of doing write-ups.

I think these write-ups are really valuable, because you can go through that in minutes instead of listening to a podcast episode in an hour, and some people like myself are just much better at taking up information via text than via a podcast.

Leave a comment to let me know what you think.

So, here's the first one…

If you like this newsletter, please consider subscribing and sharing it or forwarding it to others who might be interested. I'm also on Twitter @fxmacroguy if you want to reach out.

Release date: 05.08.2022

Host(s): Imran Lakha

Guest(s): Andreas Steno, Brent Kochuba, Darius Dale, Tony Greer

No charts were included in the video, all charts were added by me.

Notes

Imran does a quick walk-through of what happened since the Q2 roundtable:

S&P dropped from 4.600 to 3.650 before the recent bounce

Bonds have been a bit more receptive to recession concerns, further inversion of the 2s10s curve

Commodities have seen wipeouts in ags and metals. Energy has been a bit more resilient

Dollar wrecking ball has been in play

Energy has thrown Europe into stagflation, the ECB is cornered

Crypto has been dragged down by macro weakness and financial conditions tightening

The guys’ macro views

Darius’ view: The inflation cycle upturn has been more aggressive and more protracted than expected. As a consequence we're now in a liquidity, growth and earnings estimates downturn that's likely to be deeper and more protracted than what is expected. The outlook for risk assets is therefore unfavourable, and he does not believe the lows are in.

Andreas’ view: This is currently the biggest interest rate shock in modern history, and interest-rate sensitivity-based models imply PMIs heading as low as 35-40. He thinks it's a no-brainer to play risk assets from the short-side because he expects growth to slow down more than currently priced in.

Has inflation peaked enough to go long bonds?

Darius and Andreas have advocated for a long bond position. Imran asks whether inflation has peaked enough to go long bonds.

Andreas answers that there's party in the front and business in the back of the yield curve with the short end is very inflation-focussed while the long end is starting to trade the slowdown in growth narrative. He believes the yield curve will invert further and likes to be long the long end. Darius adds that his long bias is because of the Fed's resolve to get inflation back to 2% target and less with inflation peaking. He thinks the recent FOMC meeting supports that view, because:

The vote for 75 bps was unanimous despite two new FOMC members and Esther George having dissented at the meeting before,

Powell was very dismissive of recession fears, and

The Fed wants growth to slow.

Tony says he agrees with what Andreas and Darius have said about the economy. From a trading standpoint he sees equities going higher before going lower:

S&P futures positioning is as short as during Covid lockdowns and during the 2015 selloff

Sentiment indicators are still very much on the fear side, also sentiment on Twitter is similar.

He believes it's a short-covering rally that has room to at least 4.300 in the S&P before it's over. His trade is commodities outperforming technology, so recent market action has been a huge retracement.

Brent says that positioning has been in place for the rally to occur. The market is now in a neutral zone as far as options positioning is concerned. Bottoms tend to come with fear and loathing, but so far it has been: when can I buy the dip? He also thinks that there's a risk-on bias right now just based on how stuff has been trading.

Imran says that in the 1970s the 2s10s spread went to -200 bps. Having a flattener on is safer than being long bonds. He expects higher volatility especially in the rates market because the Fed isn't giving forward guidance anymore.

Are metals going to be leading the way lower like in 2008?

Imran: Let's focus on commodities. There's been a bit of a flush-out in ags and metals. Are metals going to be leading the way lower like in 2008?

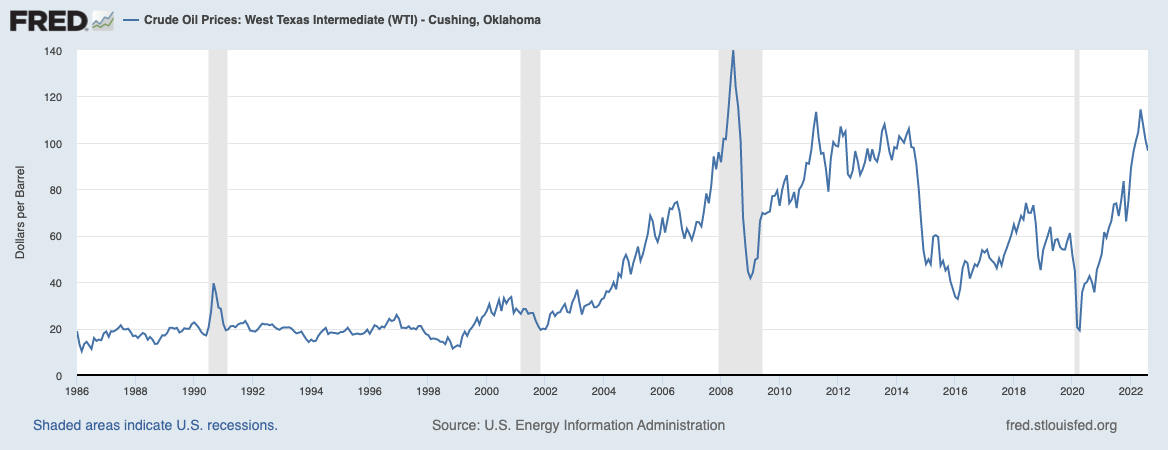

Tony says there's a battle around how slow the economy is going to be for how long. Energy has pulled back but it doesn't want to break below support:

There's no spare capacity to control upside in price: OPEC spare capacity is limited, Saudi rig count is down to 31 from normal around 75

Gasoline open interest has fallen to lowest levels in 10 years, no speculator positioning on the long side

Gas demand is strong, currently record demand in the US

He says his gut feel is that the market is going to break down, but it's really a battle between the physical markets and the perception of where markets are going. But: inventories are low, spreads are in backwardation and energy policy heading to net zero will cause energy markets to remain super tight. Plus, there's going to be a “Battle Royale” between Russia and Europe in the winter, so he maintains his long bias on energy.

Imran asks why agricultural commodities have been destroyed when natural gas feeds into fertilizer prices and the food supply. Tony says that ammonia prices have barely budged and are still up 8-10 times, so it's very difficult to reconcile the currently low grain prices. Andreas adds that there's a time lag between the price of natural gas, fertilizers and food prices. Gas prices in Europe are up by a factor of about 10 since December and energy demand is extremely inelastic. Electricity is up by 1,000% while usage is down 2.5%. So even if price explodes people will still consume energy.

Darius believes that inflation is going to be much lower a year from now, but it's unclear if it's going to be 2%, 4% or 6%. The Fed's guidance says 2.7% Core PCE by the end of next year, so about 210 bps lower than in June. That has never happened in the past without going through a recession, especially since structural changes are shifting inflation higher:

Deglobalization,

Under-supply of labour particularly in the US, and

Structural under-supply of commodities.

These things aren't going to go away until the end of next year, so it's likely the Fed has to tighten for longer.

He adds that we've seen crude oil prices rise through three of the past seven recessions: 1973-75 with the OPEC oil embargo, 1980 and 1990-91, and it rose for the first eight months during the GFC.

What's the outlook on the dollar?

Imran asks whether the pullback in the dollar is just a pullback and what the outlook is on the dollar.

Andreas answers that he's very positive on the dollar. There are two dollar liquidity sources: the Fed and global trade (US exporting dollars via negative trade balance). If global trades shrinks over the next couple of quarters and the Fed is tightening it's going to be bullish for the dollar vs. most other currencies.

Darius says he likes short EURUSD for a couple of reasons: Europe is heading into a recession and there are secular shifts in terms of trade in favour of the USD vs. the EUR.

Imran has been a seller of EUR for months, but he's surprised the BTC-Bund spread has stopped breaking higher.

Andreas thinks the ECB won't use the TPI but the old tools instead where they shift reinvestments from PEPP towards Italy, and they are not going to tell us. The question is to what extent Germany is willing to accept it. He thinks they accept it for now because of the geopolitical and energy situation in Europe at the moment. Tony is very bearish EUR especially when Europe is at the mercy at Vladimir Putin this winter. He envisages a scenario with massive unrest and even higher pressure on the EUR than right now, and he wouldn't be surprised by a complete breakup of the EU. Imran thinks it's possible for EURUSD to be at 0.80 at the end of the year.

Imran says that the other thing driving the dollar is the yen and he's asking for thoughts on it. Andreas believes it's still a good trade to be long the JPY, especially vs. the Euro. The BOJ will receive a tailwind if he's right on his growth outlook.

Darius looks at his model and estimates that USDJPY is either 5 big figures too overpriced or the US treasury yield that is about 50 bps underpriced.

Could crypto be a leading indicator out of the current bear market?

Imran asks what the guys think of crypto after the flush-out.

Darius agrees with the view that Bitcoin has been a leading indicator historically, because it's completely free-trading. Its leading properties are mostly at the highs, though, and he doesn't think it's going to be a particularly good leading indicator at the bottom. He believes that there's more downside in crypto because of the liquidity cycle.

Andreas bought crypto when he left investment banking, and he bought it at the peak. He thinks crypto has the highest beta with regards to the liquidity cycle. Tony sees it as a levered bet on risk assets, believes it's going to go lower to around 10k. Brent thinks that there isn't a case for large crypto adoption. Imran doesn't see Bitcoin as an inflation hedge but a hedge against monetary debasement: it's going up when asset prices are rising, but when you have actual inflation it's not performing. He agrees that we haven't seen a bottom in crypto, yet. The Ethereum merge could be a short-term catalyst for more upside. Darius points out that there's still a lot of regulatory risk.

Can the market rally if everyone expects a Fed pivot?

Imran: And when the Fed is done, what are you guys buying?

Andreas believes financial conditions need to be tighter to have a recession, so the Fed will need to do more in the short-term and they will need to do more than is priced in. Fed speakers have been trying to communicate that, because they want demand destruction. After the Fed pivot he thinks ARKK will be performing again.

Darius thinks equity markets aren't pricing in a recession at current valuations. He believes that the market isn't able to discount far enough into the future.

Tony believes the Fed pivot is going to be kept in check by commodities. He can easily see oil being back above $100, energy remaining super tight and headline inflation not dipping much below 8%. It's hard for him to even get to a Fed pivot. A possible easing cycle is too far ahead for him to consider it.

In Brent's opinion the beaten-down tech stocks could rebound because of short-covering. Imran adds that in the latest bounce you would have thought ARKK would outperform: crypto ripping up hard, bonds ripping up hard, but ARKK isn't going up. People want high-quality tech because people don't think the bottom in the market is in.

Is equity vol just a useless hedge or do you expect a better performance from equity vol in the second half of the year?

Brent thinks that unless there are major credit issues and defaults there won't be a 60-handle VIX. The market feels that vol is grinding lower when there's a selloff. Imran believes that people were well hedged, possibly with put spreads, so dealer's weren't caught with short vol on the way down, so they didn't have to bid up volatility. He thinks there needs to be more complacency in the markets for vol to spike. In the first 10% down from here he doesn't think vol is going to go crazy, but more on the next 10% after that. Tony is buying the dip in the S&P, because he thinks we can rip higher, but he wants to be long vol from a tactical point. Brent points out that there are individual stocks that can fall precipitously, he mentions the ARKK basket with stocks that have seen a lot of short-covering but don't really have a business case. Imran: S&P vol is a broad basket. When MOVE was at its highs the S&P vol wasn't doing much, because the volatility was going on in the form of sector rotation. Rates vol and FX vol are probably going to be moving more than the VIX.

Brent asks Darius about the MOVE and whether we can see equities higher as long as the MOVE isn't going lower. Darius responds that the Fed speakers pushed back against market interpretations of a Fed pivot and that led to a full 25 bps move higher in the terminal rate expectations in a single day. There was barely an impact in risk assets. That means that there's investors pushing back into equities. He's tracking the VVIX/VIX ratio.

Normally, in a bear market that's going lower because VIX is spiking faster than VVIX. This year it has been kind of the opposite: the VVIX is going down faster than the VIX. He thinks it's an indication that market participants have taken down a lot of risk. Imran thinks that the general consensus is that the VIX isn't going below 20, so put flow in the VIX has changed because no one wants to buy VIX puts any more. That keeps VVIX suppressed.

Darius has looked at the 17 bear markets since the Great Depression, and the market usually doesn't bottom before the inflection point of the liquidity cycle: typically it bottoms one month after and in an inflationary bear market three months after the low of the liquidity cycle.

What are you buying when things turn around?

Tony is already long because he's trading short-term: natural resources, fertilizer stocks, covered retail shorts and Q's short. Preparing to re-enter shorts around 200-day moving average, thinks towards the autumn markets are going to fall again.

Darius thinks you want to buy defensive assets if you think the June low is holding. If you think this is just a bear market rally then he favours a short-dollar trade three to six months from now.

Is the bottom in yet?

Darius: no.

Tony: no, “but it's in for now for me” because he's on an hourly timeframe.

Brent: no.

Imran: also no.

Great, that someone started doing transcripts! There are so many podcasts, but so little time. And readingis much faster/much more time efficient!