[FREE] fx:macro Lite / 24.09.23

Week in Review and the second part of our Term Structure Primer

Hi there! It's already Sunday, so welcome to fx:macro Lite! I hope you had a great trading week and could take advantage of the volatility!

If you want to know what’s up with the oranges in the cover image, we’ll get to that in the second part of our primer on the term structure below.

In case you missed the usual deep-dive yesterday, you can still sign up for that here and get access to the premium content:

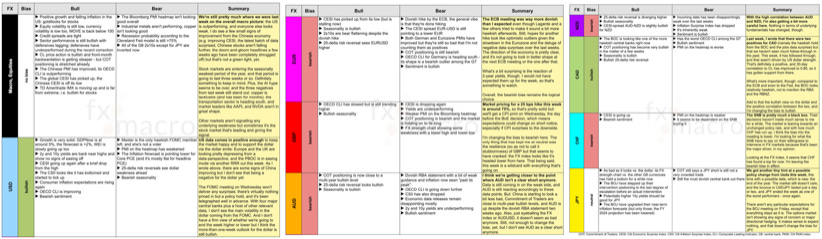

💎 Week in Review

We had four central bank meetings this week, two central banks released their meeting minutes, and we got a dump of PMIs on Friday. Here's a review of all these events. If you're trading forex, reading the central bank material is pretty much basic homework, and if you're an investor, reading through the PMIs is a great way to gauge what's going on in the economy.

Here's a sample of what it looks like, and the link to the full PDF is below.

fx:macro Premium includes a review like this every week plus a ton of relevant research. You can find out more about it here:

📌 Here's something useful

💡 Term Structure Part 2: How to use it

If you missed the first part, you can give it a quick 5-minute read here:

[FREE] fx:macro Lite / 17.09.23

![[FREE] fx:macro Lite / 17.09.23](https://substackcdn.com/image/fetch/$s_!vHR2!,w_280,h_280,c_fill,f_webp,q_auto:good,fl_progressive:steep,g_auto/https%3A%2F%2Fsubstack-post-media.s3.amazonaws.com%2Fpublic%2Fimages%2Ff783421b-2902-40a4-9919-85fcdaeef77c_1024x1024.png)

Hi there! It's already Sunday, so welcome to the first edition of fx:macro Lite! I hope you like the new format. If you missed the usual deep-dive yesterday, you can still sign up for that here and get access to the premium content: 💎 FOMC Meeting Prep for next week

Before we get to the juicy part, here's the answer to the question from last week: how are the far-out futures contracts priced when they had zero trades (and thus, zero volume)?

🐇 A Small Rabbit Hole on Settlement Rules

Unsurprisingly, there's an impressive set of rules that goes into determining the settlement price. Here's an example for ZC, the corn future. If there were no trades in a contract, they will look at trades in adjacent expirations and use that to figure out a reasonable price:

If that doesn't work, they will just change the price by as much as the neighbouring nearer-term contract:

While I don't think knowing this is an absolute must, it's still a good reminder that exchange (and product) rules exist, and it's better to know them than not to. Just think of CL trading into negative prices in 2020 or the XIV blowup during the Volmageddon episode of 2018.

📐 Measuring the Futures Curve

Okay, so let's get to the (hopefully) more interesting parts. Before we look at trading with it, we must first figure out how to measure the term structure. I'll show you two ways and their pros and cons:

Using a linear regression line through the term structure, and

Comparing two (or more) single points on the curve.

🧮 Linear Regression

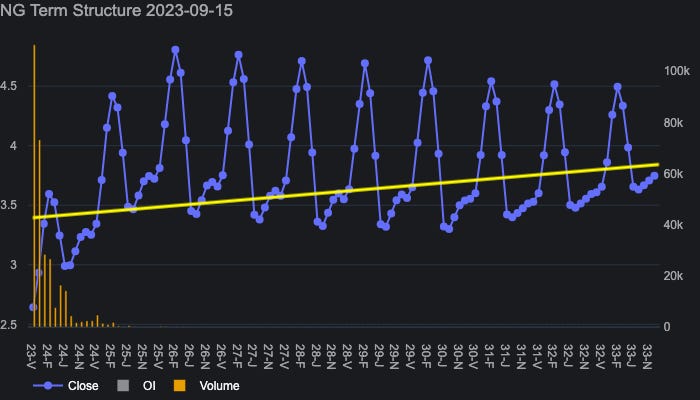

I'm happy to say that there's no maths in this paragraph! Look at the following chart with the term structure of NG, natural gas:

Linear regression is a mathematical way of figuring out the slope of the yellow line when the number of points on either side of the line and their distances from it are equal. That gives us one handy number to work with for every trading day: the slope of the linear regression line. Positive = contango, more positive = steeper contango, negative = backwardation, more negative = steeper backwardation.

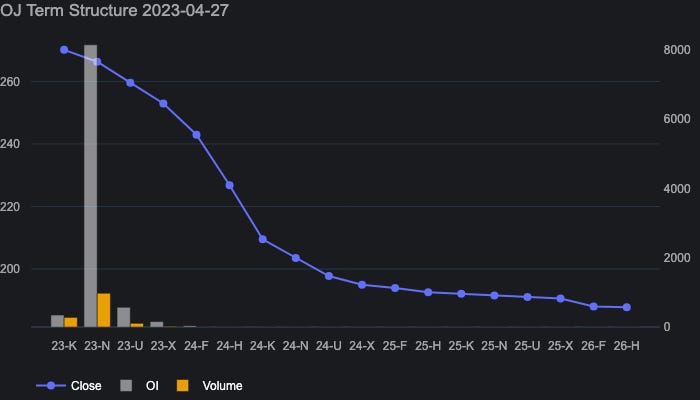

Have a look at the following chart where you can see the price of OJ, orange juice, in blue (right-hand scale), and the slope of the linear regression line in grey (left-hand scale, inverted). When the term structure gets more into contango, this line will fall (because of the inverted scale), and when we go more into backwardation, it will rise.

There are a few things to note:

Price and the slope of the term structure go together,

We're deep in backwardation right now (the slope is at around -3 or so), and

There's a divergence: the price of OJ has gone up while the term structure has flattened.

A divergence like this is bearish for OJ, which must make happy considering he bought puts on OJ a while ago:

That divergence is something you can't see by just eyeballing the individual expirations. The following two charts illustrate this: the first one is from the day when the backwardation was at its extreme, and the second one is more recent. I can't see which one is more and which one is less steep here.

The linear regression metric is objective and tells the story. The bad thing is: it's not widely available, let alone on TradingView. I'm sure there are better ways to look at it but it's always good to remember there's probably no “correct” way of doing things like this but rather a hundred different ways that all lead to Rome.

⚖️ Comparing two points on the curve

So, what we need now isn't something “more perfect” or “better” but something applicable that's available and easy to use.

Have a look at the following chart from TradingView: you can see CL1!, the CL front month future. The blue line is CL1!-CL2!, which just takes the difference between the front month and the next expiration. That's nothing else than the steepness of the curve between those two points, i.e. “front-month contango.” And it works quite well:

💸 Banking with the Term Structure

The bad news first: we're already past the 5-minute reading time mark - but the good news is that next week is another week to bring this little series to a close.

There are a few more things to go over: what are the pitfalls of the simplified TradingView approach, what are practical examples and how does it work for weird term structures like NG.

Feel free to leave a comment and let me know what you think!

Cheers,

FXMG

PS. Sorry for the cliffhanger again… but it is what it is.

How do you put the ADR etc into the TV Charts?

I am but everyone is still waiting for hurricanes to flatten Florida!!